Share on

What Are International Payments? How They Work, Types, Costs & Business Guide

International commerce increasingly depends on the ability to move money across borders, enabling businesses to serve customers in different countries and operate globally.

For example, a SaaS company billing users across regions, an ecommerce merchant selling internationally, or a marketplace paying global sellers all rely on cross-border payment flows to operate.

However, international payments are more complex than domestic transactions because they operate across multiple financial systems, currencies, and regulatory environments, requiring interconnected payment infrastructures to complete a single transaction.

This guide explains what international payments are, how global payment systems work behind the scenes, the main types of payment methods, and how businesses can optimize cross-border payment performance.

Table of Contents

- What are international payments?

- How international payments work

- Payment methods and systems

- Costs and challenges

- How to optimize payments

What Are International Payments?

International payments are financial transactions where the payer and the recipient are located in different countries. These payments often involve different currencies, banking systems, payment methods, payment networks, regulatory requirements, and settlement processes.

Unlike domestic payments, international payments often move across borders through multiple financial institutions, involving currency conversion, payment routing, and compliance checks across different jurisdictions.

International payments vs domestic payments

International payments and domestic payments both move money from one party to another, but international payments involve more layers of complexity.

Key differences between domestic and international payments

|

Factor |

Domestic Payments |

International Payments |

|

Currency |

Typically processed in a single local currency |

Involves multi-currency processing and FX conversion across markets |

|

Regulation |

Governed by a single domestic regulatory framework |

Subject to multiple regulatory and compliance requirements across jurisdictions |

|

Processing |

Operates within local banking and payment networks |

Routed through cross-border banking systems, card networks, processors, and payment rails |

|

Cost |

Generally lower with predictable domestic fees |

Includes FX spreads, cross-border fees, intermediary bank charges, and settlement costs |

|

Speed |

Typically faster due to local clearing systems |

Varies by method; may involve delays due to intermediaries and compliance checks |

|

Risk |

Lower complexity in fraud and compliance management |

Higher exposure to fraud, FX volatility, chargebacks, and regulatory risk |

|

Customer experience |

Naturally localized within domestic payment methods |

Requires intentional localization of payment methods and checkout experience |

|

Reconciliation |

Simplified single-currency reporting and reconciliation |

More complex multi-currency reconciliation across providers, methods, and regions |

For example, a customer in Germany may buy a product from a merchant in Singapore. The customer pays in euros, the merchant may price products in US dollars, and settlement may happen in Singapore dollars. A single checkout transaction may involve payment authorization, FX conversion, routing, fraud screening, clearing, settlement, and reporting.

International payments can happen through many methods, including card payments, bank transfers, digital wallets, local payment methods, online payment platforms, real-time payment rails, foreign exchange providers, international checks, money orders, and crypto transfers in selected use cases.

For businesses, international payments are not only about receiving money from another country. They are about helping customers pay in familiar ways, reducing failed payments, managing currency exposure, controlling costs, and keeping global payment operations visible.

Understanding international payments is therefore not only about defining the concept but also about understanding the ecosystem that enables global financial flows.

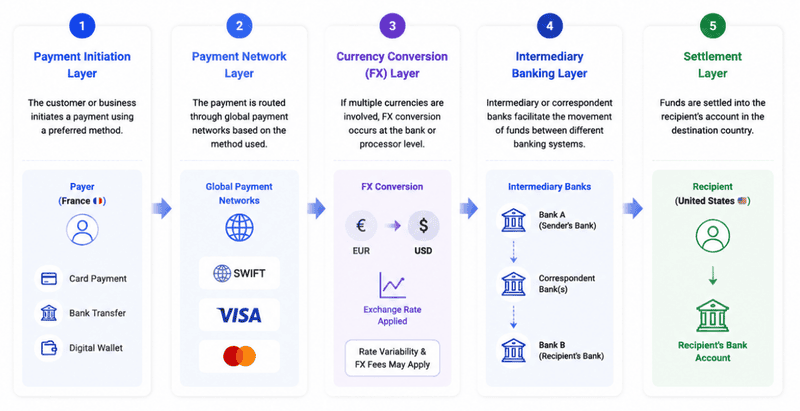

How international payments work

International payments are processed through a multi-layer financial infrastructure, where several systems work together to move, convert, and settle funds across borders.

At a high level, the process typically involves five key components:

- Payment initiation layer

- Payment network layer

- Currency conversion (FX) layer

- Intermediary banking layer

- Settlement layer

Payment initiation layer (you make a payment)

You (as a customer or business) pay using:

- a card

- a bank transfer

- a digital wallet

You are telling the system “I want to send money.”

Payment network layer (The payment is sent into the global network)

Next, the payment needs to figure out where to go.

Depending on the method:

- Bank transfers go through SWIFT

- Card payments go through Visa / Mastercard networks

The payment enters the global “messaging and routing system” that connects banks.

Currency conversion (FX) layer (The money may be converted to another currency)

If the sender and receiver use different currencies:

- EUR may be converted into USD

- or USD into another currency

The money is “changed” into the currency the other side needs. This is where exchange rates and FX fees come in.

Intermediary banking layer (The money may pass through middle banks)

Sometimes the money does not go directly to the final bank. It may pass through one or more intermediary banks.

They make the system work globally, but may also:

- charge extra fees

- slow things down

These are “middlemen banks” that help move money between countries.

Settlement layer (The money finally arrives)

At the end of the process, the money reaches the recipient’s bank account in the destination country.

This is the moment the merchant or supplier actually gets paid.

Depending on the method:

- It can be instant (local payment systems)

- or take a few days (traditional bank transfers)

Overall, the process is influenced by:

- Payment method selection

- Currency conversion mechanisms

- Banking network structure

- Regulatory compliance requirements

- Intermediary processing steps

The complexity of this workflow is one of the primary reasons why international payments are more expensive and slower than domestic transactions. Usually, the more intermediaries involved, the higher the cost and slower the settlement.

Payment methods and systems

Types of International Payments

International payments can be executed through several different methods, each designed for specific business needs, transaction sizes, and market environments.

Bank Transfers (SWIFT)

Bank transfers are one of the most traditional forms of international payments and are typically processed through the SWIFT network and correspondent banking systems.

Best for:

- High-value B2B transactions

- Supplier payments

- Corporate treasury transfers

Key advantages:

- Globally accepted across nearly all banking systems

- Suitable for large transaction amounts

- Strong documentation and audit trail

Limitations:

- Multiple intermediary banks may be involved

- Higher transaction and FX-related fees

- Slower settlement times (1–5 business days)

Credit Card Payments

Credit cards are widely used in international ecommerce transactions and are processed through global card networks such as Visa and Mastercard.

Best for:

- Ecommerce checkout

- Subscription services

- Travel and digital goods

Key advantages:

- Fast and seamless checkout experience

- Instant authorization

- High global acceptance rate

Limitations:

- Cross-border interchange and FX fees

- Higher processing costs for merchants

- Chargeback risk

Debit Card Payments

Debit cards function similarly to credit cards but are directly linked to a customer’s bank account.

Best for:

- Everyday consumer payments

- Budget-conscious users

- Markets with strong debit penetration

Key advantages:

- Lower credit risk compared to credit cards

- Widely accepted in most markets

- Direct fund deduction improves payment certainty

Limitations:

- Still subject to international processing and FX fees

- Lower flexibility for delayed payments or credit-based purchases

Digital Wallets

Digital wallets such as PayPal, Apple Pay, and regional wallet providers enable users to store payment credentials and complete transactions quickly.

Best for:

- Mobile commerce

- Digital-first businesses

- Cross-border ecommerce checkout

Key advantages:

- Fast and frictionless checkout experience

- Reduced manual card entry

- Multi-currency support in many markets

Limitations:

- Availability varies by region

- Platform-specific fees and rules may apply

Local Payment Methods

Local payment methods allow customers to pay using domestic financial infrastructure instead of international card networks.

Examples:

- SEPA (Europe)

- UPI (India)

- Pix (Brazil)

Best for:

- Localized ecommerce expansion

- High-conversion checkout optimization

- Emerging and mobile-first markets

Key advantages:

- Higher authorization and success rates

- Lower checkout friction for local users

- Strong consumer trust

Limitations:

- Fragmented across markets

- Requires local integration and support

FX & Remittance Services

Foreign exchange and remittance services specialize in cross-border money movement and currency conversion, often outside traditional card or banking rails.

Best for:

- Bulk international transfers

- Recurring supplier or payroll payments

- Currency conversion optimization

Key advantages:

- Competitive FX rates compared to banks

- Efficient for large or recurring transfers

- Flexible payout options in many corridors

Limitations:

- Not designed for ecommerce checkout

- Limited real-time payment capabilities

- Integration complexity for merchants

International payment systems and infrastructure

International payments rely on a global network of financial systems that connect banks, payment providers, and local payment rails to enable cross-border communication, authorization, and settlement.

SWIFT Network

SWIFT is a global messaging network that enables banks to securely send payment instructions to each other across countries. It does not move money itself; settlement happens through correspondent banking relationships.

Think of SWIFT as the global messaging app for banks.

- It doesn’t send money

- It only tells banks: “Please send this payment”

The actual money still moves later through banks behind the scenes.

SEPA (Europe)

SEPA standardizes euro payments across European countries to make cross-border euro transactions more efficient.

SEPA is like a unified payment system for Europe.

- A transfer between two European countries feels like a local bank transfer

- No complex cross-border process inside Europe (for euros)

Fedwire (United States)

Fedwire is a real-time settlement system in the U.S. used for high-value payments between financial institutions.

Fedwire is like a real-time highway for big money transfers in the U.S.

- Banks can send large payments instantly

- It’s mainly used for high-value or business transactions

Card networks (Visa / Mastercard)

Card networks enable global card payments by handling authorization, routing, and settlement between banks.

Visa and Mastercard are like a global payment switchboard.

When you pay:

- They check if your bank approves the payment

- They route the transaction between banks

- They help complete the payment

They are not banks, but the system that connects banks.

Local payment rails (Pix / UPI / Faster Payments)

Local payment rails are domestic real-time payment systems that enable instant transfers within a country.

These are country-specific instant payment systems.

For example:

- Pix in Brazil

- UPI in India

- Faster Payments in the UK

They make local transfers:

- fast (often instant)

- cheap

- simple

And when connected globally, they can also improve cross-border payments.

Together, these systems form the underlying infrastructure of international payments.

Costs and challenges

Costs of international payments

International payments involve multiple cost layers that can significantly impact business margins.

- Foreign exchange (FX) conversion

Businesses are typically charged a spread above the mid-market exchange rate, meaning they do not receive the real market FX rate when converting currencies. - Transaction fees

Banks and payment processors charge fees for processing cross-border payments, and these vary depending on the payment method, currency, and region. - Intermediary bank fees

Payments routed through correspondent banking networks may pass multiple intermediary institutions, each potentially adding additional charges. - Payment method fees

Different methods such as cards, bank transfers, or digital wallets may include varying processing or scheme-related fees that affect total cost. - Failed payment and retry costs

Payment failures can lead to additional retry attempts, lost conversions, and increased operational overhead for merchants. - Reconciliation and operational costs

Multi-currency and multi-provider environments increase accounting complexity, requiring additional resources for reconciliation and reporting. - Settlement delays and cash flow impact

Longer settlement cycles can affect liquidity and working capital, especially for businesses operating across multiple markets. - Revenue leakage at scale

Even small percentage differences in fees or FX spreads can compound into significant revenue loss for high-volume international merchants.

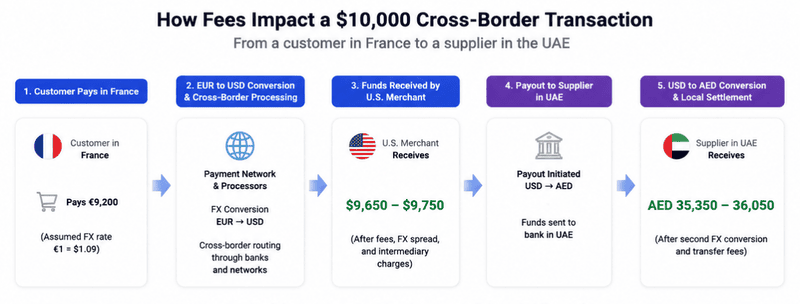

At scale, even small percentage differences in fees can result in significant revenue leakage.

For example, if a U.S. ecommerce business processes a $10,000 transaction from a customer in France, the payment may first be converted from EUR to USD, then routed through multiple cross-border systems. After processing fees, FX spreads, and intermediary bank charges, the merchant may receive only around $9,650–$9,750 in settlement.

If the same transaction is later paid out to a supplier in the Middle East—for example, in the UAE—the funds may be converted again into AED, introducing additional FX spreads and transfer fees. By the time the money completes a multi-region flow (Europe → U.S. → Middle East), the total cost of payment processing can exceed 3–5% of the original transaction value.

For high-volume businesses processing millions of dollars monthly, these small percentage differences accumulate into substantial revenue leakage across markets.

Challenges in international payments

International payments introduce several operational and financial challenges that businesses must manage effectively.

Exchange rate volatility

Currency values fluctuate constantly, which means the final amount received may be different from what was expected at the time of payment.

You never know the exact final amount until the payment is settled.

Regulatory compliance complexity

Businesses must comply with AML, KYC, and local financial regulations across multiple countries and jurisdictions.

Every country has its own rules, and you must follow all of them at the same time.

Fraud and chargeback risk

Cross-border transactions, especially card-not-present payments like online checkout, have higher exposure to fraud and chargebacks.

It is easier for fraud to happen when buyer and seller are in different countries.

Settlement delays

Differences in banking systems, intermediary banks, and regional operating hours can slow down settlement times.

The money doesn’t always arrive quickly—it can take hours or days depending on the route.

Fragmented payment infrastructure

Different countries use different payment systems, providers, and methods, which increases integration complexity for businesses.

There is no single global payment system—you have to connect many different ones.

International payments are complex because businesses must manage currency volatility, regulatory requirements, fraud risk, settlement delays, and fragmented global payment infrastructure simultaneously.

How to optimize payments

How businesses use international payments

International payments are not only a financial infrastructure component—they are a core operational capability that enables modern businesses to function globally.

|

Business model |

How international payments are used |

Key business impact |

|

E-commerce |

Accept global payments in multiple currencies and methods |

Higher conversion rate, revenue growth |

|

SaaS / Subscription |

Enable recurring billing and renewals across regions |

Stable revenue, improved retention |

|

Supply chain |

Pay global suppliers and logistics partners |

Stable cross-border operations |

|

Workforce payments |

Pay global employees, freelancers, contractors |

Efficient global payroll, compliance support |

|

Global expansion |

Support local payment methods and currencies in new markets |

Faster market entry, higher acceptance |

For e-commerce businesses, international payments allow merchants to sell products to customers across different countries and accept payments in multiple currencies. This directly impacts revenue growth and checkout conversion rates, as customers are more likely to complete transactions when familiar payment methods and local currencies are supported.

In subscription-based businesses such as SaaS platforms, international payments enable recurring billing from global users. These systems must handle multi-currency pricing, renewal cycles, and payment authorization retries, making payment reliability a critical factor for revenue retention.

For businesses operating global supply chains, international payments are essential for supplier settlements. Companies often pay manufacturers, logistics providers, or raw material suppliers located in different regions, requiring stable and predictable cross-border payment flows.

International payments are also widely used in workforce management. Many companies now employ remote workers, freelancers, and contractors across multiple countries. Paying these individuals efficiently requires support for cross-border payroll systems, often with varying tax and compliance requirements.

Finally, international payments support global expansion strategies. When businesses enter new markets, they must establish reliable payment acceptance infrastructure that aligns with local consumer behavior and financial systems. Without this capability, market entry becomes significantly more difficult and expensive.

Overall, international payments serve as the financial backbone that connects global demand with global supply.

How to optimize international payments

Optimizing international payments is critical for improving profitability, reducing operational friction, and increasing transaction success rates.

One of the most effective optimization strategies is local acquiring. By processing transactions through local financial institutions, businesses can significantly improve authorization rates and reduce cross-border rejection risk. This is particularly important in e-commerce environments where payment failures directly impact conversion rates.

Another key strategy is smart payment routing. Modern payment systems can dynamically select the most efficient processing path based on cost, success probability, and geographic performance. This helps reduce failed transactions and optimize overall payment efficiency.

Multi-currency settlement is also a critical optimization layer. By settling funds in local currencies instead of converting everything into a single base currency, businesses can reduce FX exposure and minimize conversion losses.

In addition, payment method localization plays a significant role in optimization. Offering region-specific payment methods—such as UPI in India, SEPA in Europe, or Pix in Brazil—can significantly improve customer trust and increase checkout completion rates.

|

Optimization strategy |

What it does |

Business impact |

|

Local acquiring |

Processes payments through local financial institutions |

Higher authorization rates, lower payment failures |

|

Smart routing |

Selects optimal payment path based on cost and success rate |

Improved efficiency and reduced transaction loss |

|

Multi-currency settlement |

Settles funds in local currencies instead of base currency |

Lower FX costs and reduced currency risk |

|

Payment method localization |

Adds local payment methods per market |

Higher conversion and better user experience |

|

Unified payment infrastructure |

Centralizes reporting and reconciliation |

Lower operational complexity and better scalability |

Finally, unified payment infrastructure helps businesses manage international payments more efficiently by consolidating reporting, reconciliation, and transaction visibility across multiple markets. This reduces operational complexity and improves financial control at scale.

How Antom Payments can help

As businesses scale globally, managing international payments through fragmented systems becomes increasingly inefficient. Modern enterprises require a unified infrastructure that can support multiple payment methods, currencies, and markets while maintaining high performance and compliance standards.

Antom provides a global payment infrastructure designed to support both SME merchants and enterprise-level businesses operating across international markets.

For SMEs, Antom offers seamless integration with leading e-commerce platforms such as Shopify and WooCommerce. This enables merchants to quickly enable global payment acceptance without complex technical integration. By supporting 300+ payment methods and 140+ currencies, Antom helps improve checkout conversion rates and reduce cart abandonment.

For enterprise businesses, Antom provides advanced payment capabilities including global acquiring, intelligent payment routing, and multi-country settlement infrastructure. These features enable businesses to optimize authorization rates, reduce cross-border payment costs, and scale operations across multiple regions efficiently.

In addition, Antom provides a unified API-based architecture that simplifies integration across different markets, along with risk management and compliance support to ensure secure and reliable global payment operations.

By consolidating payment infrastructure into a single platform, Antom helps businesses improve payment success rates, reduce operational complexity, and accelerate global expansion.

FAQ

What are international payments?

International payments are financial transactions where money is transferred between parties located in different countries, often involving currency conversion and cross-border banking systems.

How do international payments work?

They typically involve payment initiation, FX conversion, processing through global payment networks, possible intermediary banks, and final settlement in the recipient’s account.

What are the main types of international payments?

Common types include bank transfers (SWIFT), credit card payments, debit card payments, digital wallets, local payment methods, and FX remittance services.

SUMMARY

International payments are a foundational infrastructure layer of global commerce, enabling businesses to operate across borders, serve international customers, and manage global financial flows.

However, they also introduce complexity in the form of FX costs, regulatory requirements, fragmented systems, and operational inefficiencies.

Modern payment platforms help businesses overcome these challenges by unifying payment infrastructure, optimizing routing, supporting local payment methods, and improving transaction success rates at scale.