Share on

Digital wallets are increasingly becoming one of the most popular payment methods among consumers in Taiwan, China. In 2023, the total transaction value of digital wallets in Taiwan, China reached USD 5.06 billion, of which USD 308 million came from non-card-linked digital wallet transactions. By 2028, the market is projected to grow to USD 8.27 billion, at a compound annual growth rate (CAGR) of approximately 10.3% between 2023 and 2028, reflecting the strong momentum of the digital payment market.

Amid the rapid development of the payment landscape, JKOPay has emerged as one of the leading mobile payment platforms in Taiwan, China. Since its launch in 2015 by JKOS Network Co., Ltd., JKOPay has played a significant role in advancing the local digital payment ecosystem. In 2018, JKOPay obtained its electronic payment licence, and in the following year achieved comprehensive coverage of everyday payment scenarios in Taiwan, China, including utilities, gas, tuition fees, and traffic fines. JKOPay was also among the first payment providers to integrate with the Taipei Water Department, Taiwan Power Company, and the Bank of Kaohsiung's tuition payment platform. In 2019, the number of JKOPay users exceeded 4 million, accounting for 40% of the total digital payment users in Taiwan, China at that time, with average daily transaction volume reaching 1 million transactions, ranking first across the market. In 2020, JKOPay became the first digital payment institution in Taiwan, China to offer cross-border payment services, marking a significant expansion of its business scope.

Currently, JKOPay provides local users with a wide range of services, including online and offline payments, transfers, utility bill payments, investment and lending services, public transportation, taxi hailing, and food delivery. The platform has accumulated over 5.9 million registered users and established partnerships with more than 250,000 online and offline merchants, creating an extensive service network.

One of JKOPay's key strengths lies in its payment flexibility. Users can link multiple bank accounts and credit cards (it supports more linked banks and credit cards than any other electronic payment provider in the market) or make payments directly through wallet balances. This multi-channel support allows users to complete transactions quickly across convenience stores and other consumption scenarios without needing to switch payment methods between merchants, significantly enhancing convenience and efficiency.

Properties

The following table lists the product properties supported by JKOPay:

|

Payment type |

Digital wallet |

||

|

Funding source |

Wallet balance |

||

|

Acquirer |

AntomSG, AntomUS, AntomEU, AntomUK, AntomHK |

Merchant entity location |

SG, HK, US, EEA, UK |

|

Payment flow |

Redirect |

Refund |

✔️ |

|

Buyer country/region |

Taiwan, China |

Partial refund |

✔️ |

|

Time to return payment result |

Real-time |

Chargeback/Dispute |

❌ |

|

Processing currency |

TWD |

Refund period |

365 days |

|

Minimum payment amount |

TWD 1 (No fractional cents applicable) |

Default timeout |

14 minutes |

|

Maximum payment amount |

Non-KYC compliant users:

KYC users:

|

||

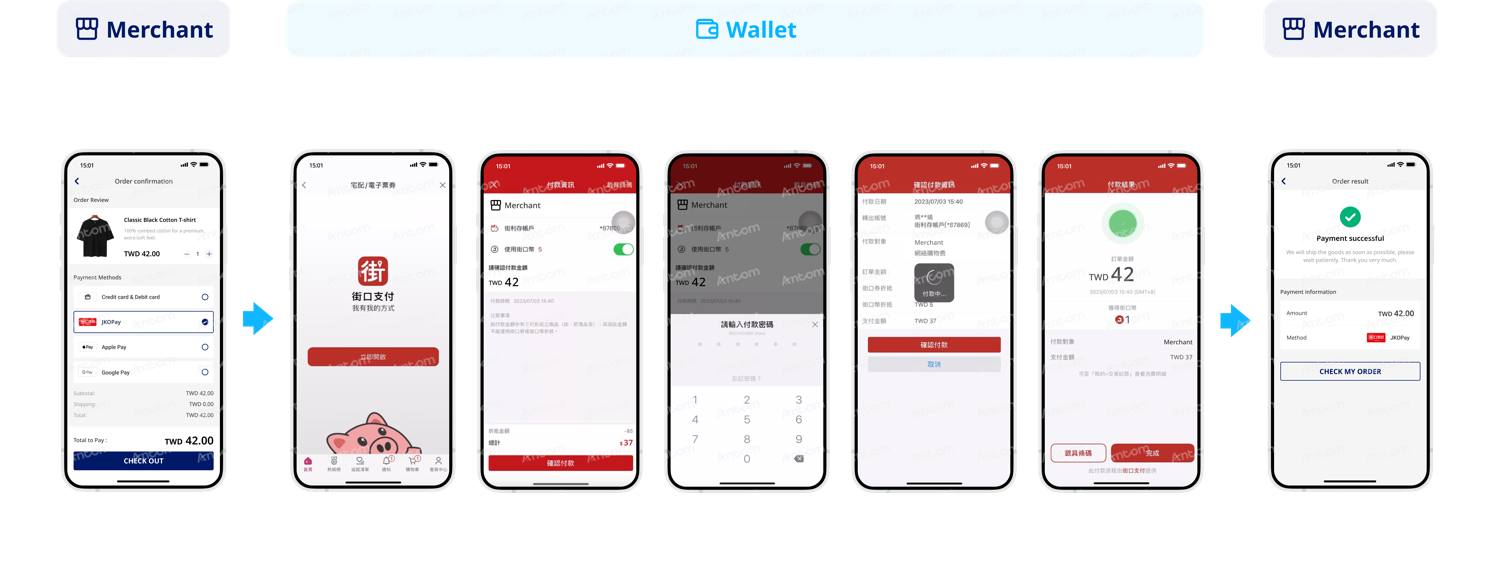

User experience

Note: The following payment flows on different terminals are for reference only. For supported merchants' terminal types, consult Antom Technical Support.

The following screenshots show the journey of paying with JKOPay on different terminals:

Web

APP

APP

FAQ

1. What are the digital payment preferences of consumers in Taiwan, China?

Consumers in Taiwan, China demonstrate clear preferences in digital payment usage across both payment methods and consumption scenarios.

In terms of payment methods, QR code payments are the most widely preferred, accounting for nearly 70% of usage. Their popularity is driven by low implementation costs, ease of use, and the frequent promotional campaigns offered by payment platforms, all of which closely align with local consumer habits. Contactless payments, meanwhile, are more commonly used in transportation systems and department stores.

In terms of consumption scenarios, QR code payments are primarily used for dining, e-commerce, convenience stores, and utility bill payments, with relatively lower average transaction values. Contactless payments, by comparison, are more commonly associated with mid- to high-value purchases.

Across demographics, consumers aged 20 to 50 (core spenders) predominantly favour QR code payments, while consumers aged 60 and above tend to prefer contactless payment methods.

2. Why do consumers in Taiwan, China trust JKOPay?

-

As a digital payment institution regulated by the Financial Supervisory Commission (FSC) in Taiwan, China, JKOPay must comply with strict requirements for user identity verification, risk control, and consumer protection mechanisms.

-

JKOPay implements a real-name registration system. When linking financial instruments such as bank accounts, users shall complete identity verification to confirm ownership. In addition, every transaction requires payment authentication through methods such as PIN codes, fingerprint recognition, Face ID, or pattern passwords. These multi-layered security mechanisms effectively protect user accounts and reduce the risk of unauthorized use.

- JKOPay provides centralised authorisation management. If users wish to stop subscriptions or recurring payments, they can directly manage them through the Authorised Payment Management feature. Compared to third-party payment platforms where users may need to manage linked credit card information separately across different services, JKOPay offers a unified management experience, reducing the risks associated with fragmented account information and personal data exposure, which makes payment authorisations easier to control.

3. What payment methods are available when using JKOPay?

-

Direct debit from bank accounts (no top-up required)

-

Credit card payments (one-time and installment payments)

-

JKOPay account balance payments

-

JKO Coins for payment offset (1 JKO Coin = TWD 1)

*The system automatically applies the user's preset preferred payment method at checkout, with the option to switch manually.