Share on

Japan's digital payment landscape is dominated by credit cards. Over the past decade, the rise of e-commerce has driven steady growth in the country's credit card market. In 2023, the total value of Japan's credit card transactions exceeded JPY 91.65 trillion, reflecting the market's vitality and vast potential.

The JCB Card, issued by Japan Credit Bureau (JCB), is Japan's first homegrown credit card brand. Today, it is the country's leading credit card issuer and acquirer with approximately 80% of the domestic market share. Over the years, JCB has evolved into a major global payment brand that is active in over 160 countries and regions, with a strong foothold in Asia. In fiscal year 2024 (April 2024–March 2025), JCB's total transaction volume reached JPY 50.2 trillion, with its cross-border payment business continuing to post double-digit growth.

In April 2024, JCB entered into a multilateral acquiring partnership with Antom, a subsidiary of Ant International, becoming one of the first members of Antom's Global Card Association Direct Connection Programme. The partnership aims to expand international payment scenarios and enhance cross-border transactions. In Japan, JCB's clearing system operates with exceptional efficiency, with transaction success rates far exceeding the global average.

As of March 2025, the number of JCB cardholders had exceeded 169 million. JCB's extensive reach and strong footprint in Asia, especially in Japan, make it an indispensable payment option for merchants seeking to expand across the region. Currently, more than 90% of luxury hotels, department stores, and duty-free shops in Japan accept JCB cards, providing cardholders with a seamless international payment experience. According to 2025 data, JCB's online cross-border transactions rose by 18% year on year, spearheaded by spending on luxury goods, beauty, and digital subscriptions.

Properties

The following table summarises the main features of JCB credit card payments, covering merchant acquiring, supported currencies, 3D Secure, refund options, and chargeback or dispute management.

|

Availability |

Acquirer |

2C2P HK |

AntomSG |

AntomUS |

AntomJP |

|

Merchant entity location |

HK |

SG |

US |

JP |

|

|

Buyer country/region |

Global |

Global |

Global |

Global |

|

|

Product features |

Payment type |

Card |

Card |

Card |

Card |

|

Card brand |

JCB |

JCB |

JCB |

JCB |

|

|

Card type |

No limit |

No limit |

No limit |

No limit |

|

|

Processing currency |

Refer to the Processing currency for 2C2P HK table |

Refer to the Processing currency for AntomSG table |

USD |

JPY |

|

|

Others |

3D |

✔️ |

✔️ |

✔️ |

✔️ |

|

Authorisation validity period |

7 days |

||||

|

Minimum payment amount |

The smallest unit of the acquirer currency |

0.01 USD or equivalent |

1 JPY |

||

|

Maximum payment amount |

499,999 USD or equivalent |

9,999,999.99 USD |

Unlimited |

||

|

Recurring payments (MIT) |

❌ |

❌ |

✔️ |

❌ |

|

|

Multiple partial captures |

❌ |

✔️ |

❌ |

❌ |

|

|

Partial capture |

✔️ |

✔️ |

✔️ |

❌ |

|

|

Refund |

✔️ |

✔️ |

✔️ |

✔️ |

|

|

Partial refund |

✔️ |

✔️ |

✔️ |

✔️[1] |

|

|

Chargeback/Dispute |

✔️ |

✔️ |

✔️ |

✔️ |

|

|

Refund period |

365 days |

365 days |

365 days |

180 days |

|

|

Advanced AVS check |

❌ |

❌ |

❌ |

❌ |

|

|

Special payment element |

Refer to Special payment elements for cards for more details |

||||

Note:

1. JCB credit card payments support multi-currency and cross-border transactions, offering a high authorisation rate and a secure, reliable payment experience. It is one of the most trusted and widely used payment methods across Asia and around the world.

[1] Partial refund is conditional and requires additional approval to be enabled.

2. AVS is an anti-fraud service provided by credit card issuing banks, primarily used to verify the cardholder's identity during online or card-not-present transactions.

User experience

This section shows the user experience of JCB in different scenarios:

API integration

This section shows the difference in user experience between those PCI and non-PCI qualified under the API integration.

PCI qualified

This section shows the difference between the first-time and subsequent payments under the PCI qualified.

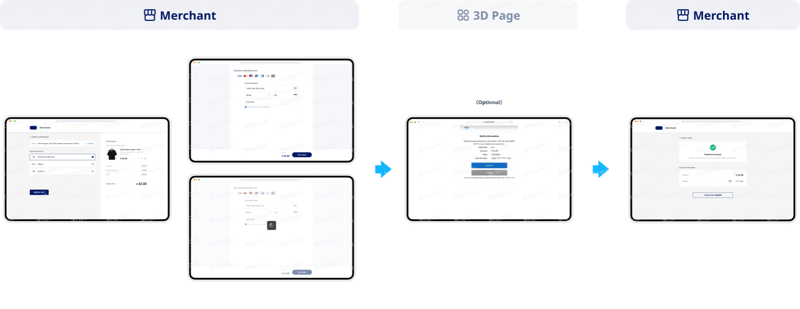

First-time payment

This section shows the difference between Web and app when making the first-time payment under the PCI qualified.

Web

App

.png?width=800&height=310&name=image%20(2).png)

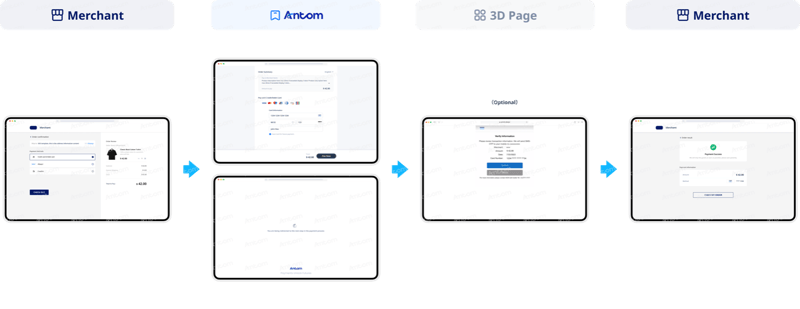

Subsequent payments

This section shows the difference between Web and app when making the subsequent payments under the PCI qualified.

Web

.png?width=800&height=310&name=image%20(3).png)

App

.png?width=800&height=310&name=image%20(4).png)

Non-PCI qualified

This section shows the difference between the first-time and subsequent payments under the non-PCI qualified.

First-time payment

This section shows the difference between Web and app when making the first-time payment under the non-PCI qualified.

Web

App

.png?width=800&height=310&name=image%20(6).png)

Subsequent payments

This section shows the difference between Web and app when making the subsequent payments under the non-PCI qualified.

Web

.png?width=800&height=310&name=image%20(7).png)

App

.png?width=800&height=310&name=image%20(8).png)

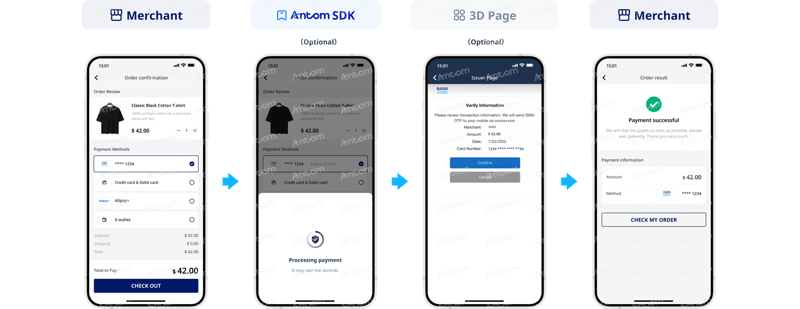

SDK integration

This section shows the difference between the first-time and subsequent payments under the SDK integration.

First-time payment

This section shows the difference between Web and app when making the first-time payment under the SDK integration.

Web

.png?width=800&height=310&name=image%20(9).png)

App

.png?width=800&height=310&name=image%20(10).png)

Subsequent payments

This section shows the difference between Web and app when making the subsequent payments under the SDK integration.

Web

.png?width=800&height=310&name=image%20(11).png)

App

By integrating with Antom and 2C2P via API, merchants can easily accept JCB credit card payments, enabling global acquiring and multi-currency settlement.

Choose JCB for Growth across Asia and the World

As Japan's only international credit card brand, JCB holds an irreplaceable position in the Asian market.

Through direct connection with Antom, and supported by advanced API/SDK integration and stringent PCI standards, JCB provides merchants with a secure and reliable experience in cross-border and credit card payments.

From e-commerce and subscription services to travel and premium retail, JCB's acquiring network empowers businesses to expand internationally with ease with enhanced conversion rates, and comprehensive transaction security.

FAQs

1. How is JCB's authorisation rates in Japan?

JCB achieves a local authorisation rate of 91.7% in Japan, around 8 percentage points higher than cross-border routing. The difference is most notable in high-value spending, such as luxury goods and hospitality. JCB's localised authorisation and security verification systems help merchants improve payment success rates.

2. Can I use JCB cards for international payments?

Yes. JCB cards are accepted by over 39 million merchants in around 190 countries and regions worldwide. Particularly in Japan, South Korea, and Southeast Asia, JCB enjoys extensive payment coverage and strong consumer recognition, making it a preferred choice for cross-border e-commerce and travel.

3. Are JCB international transactions secure?

JCB ensures transaction data security with EMV chips, 3D Secure 2.0 (for frictionless authentication), tokenisation, and the PCI-DSS industry standard that is co-developed with the world's other four major card brands.

4. Does JCB have AI-powered anti-fraud tools?

Yes. In August 2025, JCB, in collaboration with Trend Micro, launched an experimental Generative AI Fraud Detection feature. Before making international payments, cardholders can upload screenshots of suspicious emails, SMS messages, or websites for instant AI analysis and security advice, allowing users to complete international payments with confidence.

5. What is the Interchange++ pricing model?

Interchange++ is a highly transparent payment pricing model. This model accurately tracks the interchange fees and card network settlement fees incurred for each transaction, and it can calculate the cost estimate for a transaction before the payment is completed. With this precise, transaction-level pricing model, merchants can clearly understand the actual cost breakdown for each payment.

6. Does Antom charge an initial system fee or monthly service fee?

Antom's basic acquiring products do not charge any system setup fees, monthly service fees, technical integration fees, or account cancellation fees. If you would like to learn more about the specific service terms and fee structure, please contact our sales team, who will provide a customised service plan based on your business needs.