Share on

What Is a Cross-Border Interbank Payment System? CIPS, SWIFT, and Business Payments Explained

A cross-border interbank payment system is bank-to-bank infrastructure used to exchange payment instructions, clear obligations, and settle international payments. The term often refers to CIPS, China’s RMB cross-border clearing and settlement system authorized by the People’s Bank of China. It is different from SWIFT, which mainly provides secure financial messaging, and ISO 20022, which defines richer payment message data.

For global businesses, these systems help explain why international payments can vary in speed, cost, transparency, and settlement efficiency. But in most commercial payment scenarios, merchants typically do not connect to interbank systems directly. They often need merchant-facing payment solutions that support local payment methods, acquiring, risk control, settlement, and reconciliation across markets.

Key takeaways

-

A cross-border interbank payment system helps banks exchange payment instructions, clear obligations, and settle international payments.

-

The term often refers to CIPS, China’s RMB cross-border clearing and settlement system, while SWIFT mainly provides secure financial messaging.

-

For merchants, interbank infrastructure is only one layer. Businesses also need local payment methods, acquiring, routing, risk control, settlement, and reconciliation.

What is a cross-border interbank payment system?

A cross-border interbank payment system is a financial infrastructure that enables banks and financial institutions to exchange payment instructions, clear obligations, and settle funds across borders.

It is important to separate three concepts that are often mixed together:

|

Concept |

Meaning |

Simple explanation |

|

Messaging |

Sending payment instructions between financial institutions |

“Who should pay whom, how much, in which currency, and for what purpose?” |

|

Clearing |

Calculating, validating, and matching obligations between banks |

“Which bank owes what to which other bank?” |

|

Settlement |

Final movement of funds between financial institutions |

“The money is finally transferred and the obligation is completed.” |

In simple terms, this is the infrastructure banks use behind the scenes when money needs to move across borders. A business or customer may only see a payment being sent, but banks still need to exchange instructions, check obligations, and settle funds through the right financial infrastructure.

This distinction matters because cross-border payments involve different jobs: sending instructions, checking and calculating obligations, and settling funds. But not every system does all three.

For businesses, the key takeaway is simple: a cross-border payment is not just money moving from one account to another. Behind the scenes, it may involve payment messages, compliance checks, currency conversion, clearing systems,settlement accounts, and intermediary banks.

Is Cross-Border Interbank Payment System the same as CIPS?

In many search contexts, “Cross-Border Interbank Payment System” refers specifically to CIPS. CIPS stands for Cross-Border Interbank Payment System, China’s RMB cross-border clearing and settlement infrastructure.

CIPS is a wholesale payment system authorized by the People’s Bank of China and designed to support the clearing and settlement of cross-border RMB payments. In simple terms, CIPS helps participating banks process RMB payments between China and other markets more efficiently.

In some payment flows, banks may still use SWIFT messages together with CIPS, depending on the participants, currency route, and system connection.

This is why people searching for “the Cross-Border Interbank Payment System” are often looking for CIPS: how it works, how it compares with SWIFT, and how it supports the international use of RMB.

However, in a broader industry context, cross-border interbank payment systems can also refer to the networks and infrastructures used by banks to process international payments in different currencies. This broader ecosystem may include:

-

secure messaging networks such as SWIFT;

-

currency-specific clearing or settlement systems;

-

central bank-operated real-time gross settlement systems;

-

private-sector clearing systems;

-

correspondent banking networks;

-

nostro and vostro accounts used by banks to hold balances with each other.

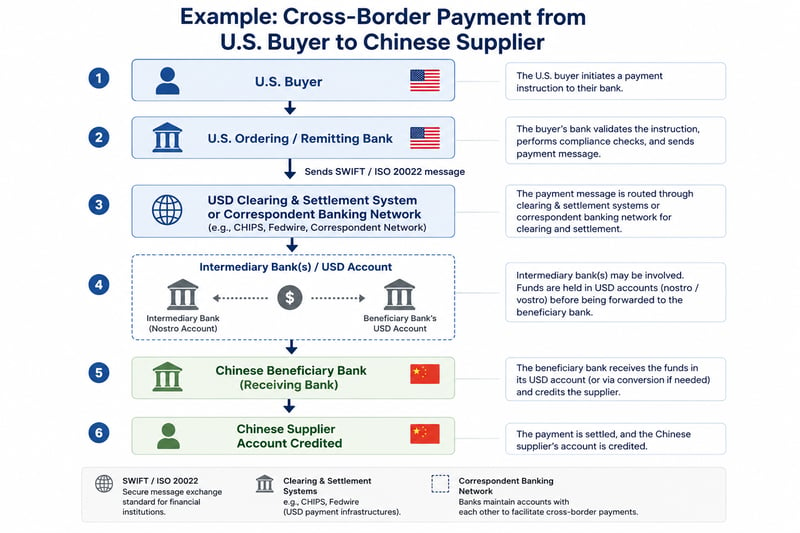

How a cross-border interbank payment works

A simplified cross-border bank payment from a U.S. buyer to a Chinese supplier may look like this:

This is a simplified example. The actual payment route depends on the currency, bank relationships, clearing access, compliance checks, and settlement rules.

USD payments may involve USD clearing systems and correspondent banks, while RMB payments may involve CIPS when participating banks process cross-border RMB settlement. In many correspondent banking flows, one or more intermediary banks are needed because the paying bank and receiving bank do not have a direct relationship. This can make some international bank transfers slower, more expensive, or harder to trace.

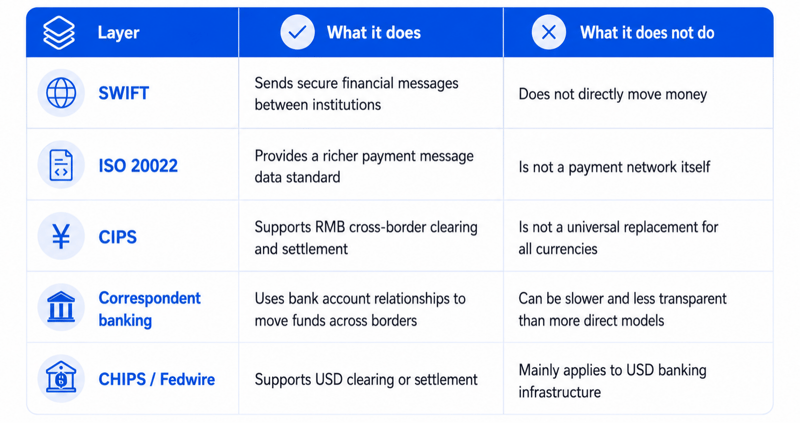

CIPS vs SWIFT vs Correspondent Banking

CIPS, SWIFT, ISO 20022, correspondent banking, CHIPS, and Fedwire are often discussed together, but they do not play the same role.

SWIFT provides secure financial messaging, whileISO 20022 defines richer payment message data. CIPS is focused on cross-border RMB clearing and settlement. Correspondent banking relies on account relationships between banks to move funds across borders. CHIPS and Fedwire are part of USD clearing and settlement infrastructure, not global messaging systems.

The key point is that a cross-border payment is rarely powered by one single system. It usually combines messaging, clearing, settlement, compliance checks, bank account relationships, and sometimes intermediary banks.

Why cross-border interbank systems matter for global businesses

Cross-border interbank systems may sound like a bank-only topic, but they affect real business outcomes:

-

Payment speed: routes, intermediary banks, time zones, bank cut-off times, compliance reviews, and local settlement windows can affect when funds arrive.

-

Payment cost: sender bank fees, intermediary fees, receiving bank fees, FX spreads, lifting fees, and compliance-related costs can add up.

-

Transparency: businesses need to know where a payment is, when it will arrive, and how much will be deducted.

-

Compliance: KYC, AML, sanctions screening, transaction monitoring, and purpose-of-payment checks can delay or reject payments when data is incomplete.

-

Reconciliation: finance teams still need to match funds to orders, invoices, customers, markets, currencies, and fees.

Geopolitical risk shows why payment infrastructure matters

The Russia-Ukraine war made cross-border payment infrastructure more visible to businesses. When sanctions restrict access to messaging networks, clearing systems, or correspondent banking relationships, businesses may face payment continuity risk, not just transaction cost risk.

For SMEs, ecommerce companies, and platforms, the practical response is not direct access to SWIFT, CIPS, or CHIPS. It is building a more flexible merchant payment layer that supports local payment methods, acquiring, routing, risk management, settlement reporting, and reconciliation across markets.

Where payment platforms fit in

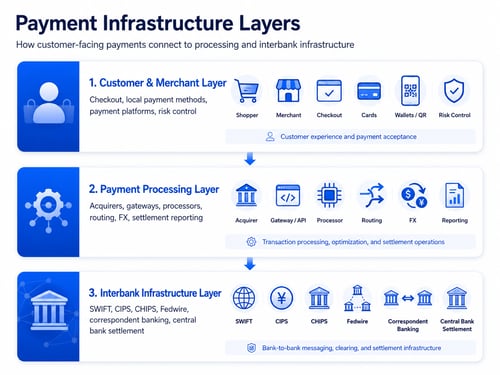

Cross-border interbank systems operate at the bank-to-bank infrastructure layer. Businesses, however, usually need a merchant-facing payment layer that handles customer payment methods, checkout experience, acquiring, routing, risk control, settlement reporting, and reconciliation.

This difference is especially important for SMEs, ecommerce businesses, marketplaces, and digital platforms. These companies usually do not want to manage direct relationships with multiple banks, local acquirers, wallets, card schemes, FX providers, and reconciliation systems in every market.

Platforms such as Antom operate closer to the merchant payment layer,offering businesses access to 200+ payment markets, 300+ payment methods, and 140+ currencies through a single gateway.

This does not mean a payment platform replaces interbank infrastructure. Instead, it helps businesses use payment infrastructure more effectively by connecting customer-facing payment acceptance with processing, local payment methods, risk management, settlement, and reporting.

The payment stack can be understood in three layers: the customer and merchant layer, the payment processing layer, and the interbank infrastructure layer.

For a merchant, the business question is usually not “Can we connect directly to CIPS, SWIFT, or CHIPS?” The more practical question is: “Can customers in each market pay easily, can payments be approved successfully, can funds be settled efficiently, and can finance teams reconcile everything clearly?”

A local payment network is not the same as a cross-border interbank payment system, but it shows why the merchant-facing payment layer matters in real markets.

Example: Cartes Bancaires in France shows why local payment access matters

Cartes Bancaires in France shows why cross-border payment infrastructure is not only about interbank settlement. CB is a French interbank card payment system and ATM network used for issuing payment cards and facilitating card transactions. It operates as a shared network for issuing banks and acquirers, helping create unified standards for card payments across French merchants. Antom’s Cartes Bancaires guide notes that CB accounts for 65% of daily transactions in France and processed 14.5 billion transactions in 2024, with EUR 700 billion in total payment volume.

For international merchants, the lesson is simple: knowing how money moves between banks is not enough to win in a local market. Customers expect familiar payment options at checkout. Merchant-facing payment platforms can help businesses support local payment acceptance, settlement reporting, risk controls, and reconciliation across markets.

Summary

A cross-border interbank payment system is essential infrastructure, but it is only one layer of global payments. Banks and settlement systems help move value between institutions. Merchants still need payment acceptance, local payment methods, routing, risk control, settlement visibility, and reconciliation to make cross-border commerce work in practice.

That is where business-facing payment platforms fit in: they do not replace interbank infrastructure, but they help businesses turn complex payment rails into a practical operating layer for global growth.

FAQs

What is a cross-border interbank payment system?

A cross-border interbank payment system is bank-to-bank infrastructure used to exchange payment instructions, clear obligations, and settle international payments. The term often refers to CIPS, China’s RMB cross-border clearing and settlement system, but it can also describe the broader infrastructure behind international bank payments.

What is the difference between SWIFT and CIPS?

SWIFT is mainly a secure financial messaging network used by financial institutions to exchange payment instructions. CIPS is China’s RMB cross-border clearing and settlement system. In simple terms, SWIFT helps banks communicate payment instructions, while CIPS helps participating banks clear and settle cross-border RMB payments.

Is CIPS a replacement for SWIFT?

Not exactly. CIPS and SWIFT serve different but sometimes connected roles. CIPS focuses on cross-border RMB clearing and settlement, while SWIFT provides global financial messaging standards and connectivity. In practice, banks may use CIPS, SWIFT, correspondent banking, and local settlement systems together depending on the currency, route, and participating institutions.