Share on

Preface

Turkey stands at the crossroads of Europe and Asia as one of the region’s most dynamic e-commerce and digital payment markets. With a population of 85 million, GDP of USD 1.32 trillion, and more than 77 million internet users, the country combines youthful demographics with deepening online engagement. E-commerce revenue reached USD 27.7 billion in 2024 and is projected to expand at a 7.5% CAGR, supported by a mobile-first consumer base and strong government initiatives such as Digital Turkey Roadmap. As credit and debit card penetration converges and new payment systems gain traction, Turkey is evolving into a strategic hub for regional commerce and financial innovation.

Key Insights

- Over 77.5% of Turkey’s population is urban, creating favourable conditions for logistics, fulfilment and digital retail growth.

- Fashion leads e-commerce spending, followed by electronics, cosmetics and homeware — all popular among Turkey’s large youth population.

- Trendyol and Hepsiburada, two domestic giants, lead Turkey’s e‑commerce market. Trendyol, backed by Alibaba, reaches 77.8% of users and operates a closed‑loop ecosystem through Trendyol Go (instant delivery), Trendyol Pay (digital wallet and financial services), Dolap (second-hand trading), and Trendyol Express (in-house logistics).

- Recent policy changes — including raising parcel tax rates for certain countries to 60% and redefining personal duty-free thresholds — are accelerating localisation, prompting cross-border sellers to shift from shipping overseas to establishing local operations.

- Credit cards account for 47% of online payments, largely due to the popularity of instalment plans (Taksit) that allow consumers to spread out costs.

- Turkey’s digital wallet market is currently led by domestic players like Papara, but new 2024 data regulations have opened the door for international payment providers.

- The growing competition in payments is expected to boost innovation and create a more dynamic digital ecosystem for merchants and consumers alike.

- International platforms such as Amazon are actively expanding in Turkey, seeking entry points within a market dominated by local leaders.

From demographics to trade: mapping Turkey’s strategic market position

Overview of the Turkish market

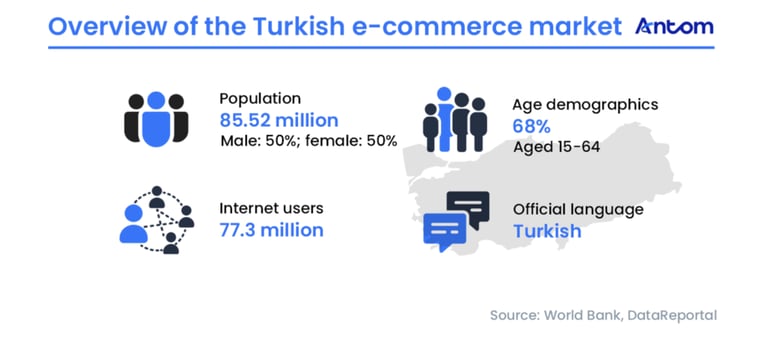

In 2024, Turkey’s total population reached approximately 85.52 million, with 77.30 million internet users. The gender distribution is balanced, and 68% of the population falls within the working-age bracket of 15 to 64. The official language is Turkish.

As a founding member of the Organisation for Economic Co-operation and Development (OECD) and the G20, Turkey holds a strategically important position on the international stage. It both serves as a bridge between Europe and Asia and is a key force in the regional economic landscape.

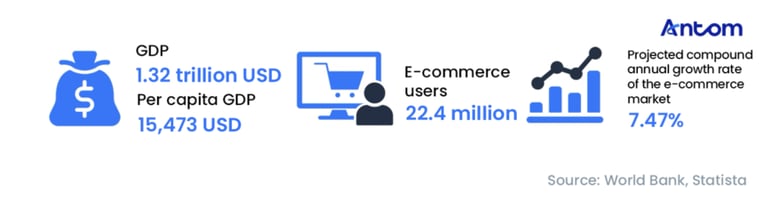

In 2024, Turkey’s gross domestic product (GDP) reached USD 1.32 trillion, placing it among the world’s top twenty economies. Per capita GDP was USD 15,473, demonstrating robust economic resilience and regional influence.

Turkey’s e-commerce market has continued to expand in recent years. The number of online shoppers reached 22.4 million in 2024 and is projected to grow to 31.9 million by 2029. According to Statista, the market’s compound annual growth rate between 2025 and 2030 is forecast at 7.47%.

In 2024, the debit card penetration rate in Turkey reached 59%, while the credit card penetration rate was 30%.

Turkey: economic overview

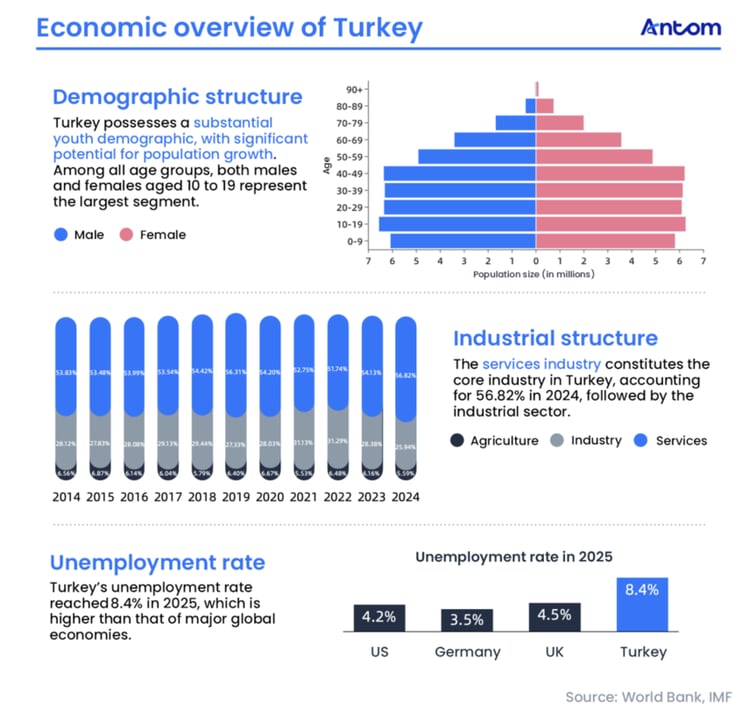

As one of Europe’s youngest countries, Turkey has a substantial base of young consumers. In 2024, the 10–19 age bracket was the largest across all age groups, providing e-commerce platforms with a large pool of potential users and long-term growth opportunities.

At the same time, Turkey is entering a phase of population ageing, with growing online demand among elderly consumers driving the rollout of e-commerce products and services tailored to senior users. Notably, women make up a slightly larger share of the elderly population, suggesting that the elder-female segment could become a new niche growth driver.

In terms of economic structure, the services sector is the backbone of Turkey’s economy, accounting for 56.82% of GDP in 2024, followed by the industrial sector. The dominance of services provides a solid foundation for the development of the digital economy and e-commerce, with particularly strong performance in areas closely linked to e-commerce such as tourism, telecommunications, and financial services. From a labour market perspective, however, Turkey’s overall unemployment rate is higher than that of the world’s major economies.

In 2024, Turkey’s merchandise imports reached $344.02 billion, with petroleum and petroleum products making up the largest share.

Data from July 2025 show that China was Turkey’s largest source of imports, and its largest trading partner in Asia, accounting for 13.4% of Turkey’s total imports.

That concludes the high-level overview of Turkey’s market. These figures should have provided a general sense of the country’s economic profile and strategic position. Next, let’s take a closer look at Turkish consumer behaviour.