Share on

Navigating the complex terrain of global commerce is rarely as simple as flipping a switch to accept credit cards. Mid-market and enterprise businesses growing internationally often encounter an unpleasant reality: authorization rates decline and checkout friction spikes. Financial and product leaders must ask: what is an acquirer, and how could our current setup negatively affect our bottom line?

An effective payment infrastructure is more than a utility; it's a key driver of growth. Antom, as an award-winning partner for digital enterprises, helps clarify this ecosystem by offering top-of-the-line acquiring services tailored to rescue lost revenue through intelligent routing and local compliance. This guide won't simply define terms; it will equip you with the operational frameworks and evaluation criteria needed to audit your payment stack, understand risks, and select partners that facilitate global expansion rather than hinder it.

What is an acquirer in Payments: Moving Beyond the Encyclopedia

The urgency to upgrade your payment infrastructure is backed by macroeconomic trends. According to Juniper Research, the global cross-border eCommerce market will exceed $3.3 trillion by 2028, representing a 107% growth from 2023. Furthermore, EY projects that the global non-wholesale cross-border payment market will expand to $65 trillion by 2030. Selecting a powerful acquiring platform is no longer optional; it is the fundamental infrastructure needed to capture this multi-trillion-dollar opportunity.

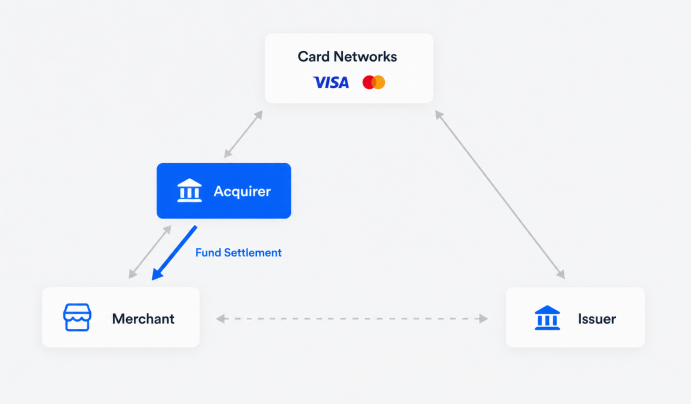

A quick definition: an acquirer (or acquiring bank) is a financial institution licensed to accept credit and debit card payments on behalf of merchants. It acts as the intermediary between your business and the Visa/Mastercard networks to make sure funds arrive safely in your merchant account.

Although accurate, this surface-level definition won't help you make sound business decisions. To truly comprehend what an acquirer in payments means for your organization, you need to examine when one actually becomes necessary.

Boundary Condition: PayFac vs. Direct Acquirer

Not all businesses require direct relationships with merchant acquiring banks for credit card processing.

- For early-stage startups: You typically utilize a Payment Facilitator (PayFac), such as Stripe or Square, as your master acquirer while acting as a sub-merchant to them. Setting this up quickly saves time but reduces control over routing, risk thresholds, and fee negotiations.

- For growing enterprises ($10M+ ARR) and high-risk models: Relying on a generic PayFac can become a liability. Sudden shifts in your risk profile can lead to unexpected account freezes. For these cases, establishing direct relationships with dedicated acquiring services becomes paramount. It provides portability of transaction data, tailored underwriting criteria, and the ability to negotiate interchange-plus pricing directly.

Payment Gateway, Acquirer, and Processor: Architectural Decisions

Understanding the differences among these three terms is only step one. Now comes the hard part: determining how they apply to your specific business model, the role each plays in the payment processing flow, and how they affect procurement strategies.

Core Components

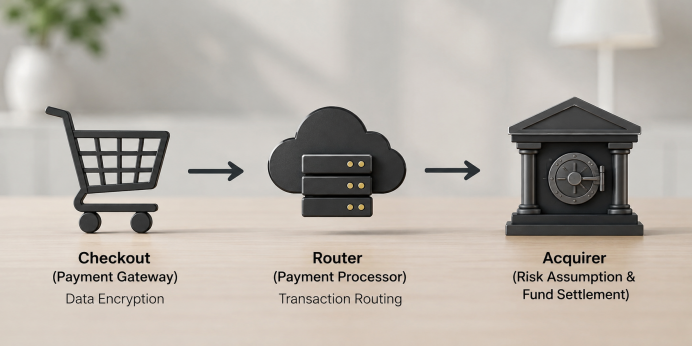

- Payment Gateway: The "checkout page API" that safely collects and encrypts card data without touching the money directly.

- Payment Processor: The technical routing engine that transmits encrypted data from the gateway to the card networks and issuing banks.

- Acquirer: The financial powerhouse. The acquirer assumes risk, manages the merchant account, and settles the actual funds.

Decision Detail: Should They Be Decoupled?

Historically, merchants sought agnostic gateways that allowed them to tap into multiple legacy acquirers simultaneously. Now, however, those distinctions have blurred. - When to Decouple: For massive volumes across multiple geographic regions, using an independent gateway may help optimize transaction acceptance by routing to several separate regional acquirers.

- When to Use an All-in-One: For most modern global platforms, choosing an integrated, full-stack provider (where the gateway, processor, and acquirer act as one entity) eliminates reconciliation headaches. Our work with top European SaaS platforms revealed accounting teams spending hours manually reconciling reports across decoupled gateways and legacy acquirers. Platforms like Antom provide an all-in-one dashboard solution, significantly decreasing operational overhead.

Assessing Your Acquiring Services: Evaluating Risk

Many businesses approach acquiring services as commodities, comparing providers purely on markup fees. To gauge an acquirer's true impact on your ROI, you must look beyond surface-level pricing and consider three hidden metrics:

A. False Declines (Authorization Rates)

Traditional acquirers use stringent fraud rules; any transaction that looks slightly suspicious may be declined to minimize the acquirer's risk exposure. For digital goods merchants, a false decline doesn't just cost a single sale—it can be fatal to customer retention.

Antom's Solution: Delivering superior acquiring services requires more than rigid rules. With Antom's Dynamic Smart Routing Engine™, transactions are analyzed using adaptive AI that takes local bank preferences into account, increasing approval rates while effectively mitigating hard fraud.Finding the perfect balance in authorization is critical. Antom's official guidelines state that maintaining a payment acceptance rate above 95% is the optimal benchmark for cross-border eCommerce. A rate close to 88% signals severe profit leakage, while anything above 98% often warns that the platform's fraud filters are too loose, inviting massive chargeback risks. Modern platforms must utilize AI-driven smart routing and auto-retry logic to dynamically distribute transactions to the most favorable local acquirers, a technology that can recover up to 15% of lost revenue caused by soft declines.B. Reserve Policies and Cash Flow Freezes

Acquirers assume the financial liability for your chargebacks. If your business involves delayed delivery (e.g., travel bookings) or subscription payments (e.g., SaaS), you are considered higher risk. An overly rigid acquirer might impose a 10% "rolling reserve" or stop payouts altogether if your chargeback ratio hits 0.9%.Risk Warning: Before signing an acquiring contract, explicitly ask about their reserve policies under stress conditions. Aim for an acquirer who will work collaboratively with you to implement 3D Secure or other chargeback mitigation tools rather than simply freezing your cash flow.

C. The MATCH List Reality

If an acquiring bank terminates your account due to excessive fraud, they may add you to the MATCH (Member Alert to Control High-Risk Merchants) list—making it nearly impossible to secure services anywhere else. A transparent acquirer provides early-warning APIs and consults closely to keep their clients off this list.Need to know if your current setup is costing you revenue? Consult Antom's risk architects for a customized payment health check to identify hidden revenue leaks and exact decline reasons. Reach out now.

The Blueprint for Cross-Border Acquiring

For globally ambitious brands, domestic payment strategies quickly become bottlenecks. When expanding overseas, cross-border acquiring is often the single greatest challenge for your finance team.

Problems With "Generic" International ProcessingWhen using a US-based acquirer to process a transaction for a customer in Brazil, the transaction is labeled as "cross-border" by the card networks. This leads to two major issues:

-

High Decline Rates: Brazilian issuing banks routinely decline foreign transactions due to complex internal fraud algorithms.

-

Exorbitant Fees: Banks often surprise their customers with unexpected foreign transaction fees, creating customer support headaches and triggering refunds.

Traditionally, achieving high authorization rates in Europe or Latin America required establishing local corporate entities, opening local bank accounts, and integrating with domestic acquirers—an impractical task for mid-market companies with limited legal resources.

The financial friction of generic processing is steep. Fortune Business Insights notes that the average global cross-border transaction cost still remains high at 6.35% in 2024, largely driven by exorbitant foreign exchange (FX) margins and intermediary fees.

Beyond fees, relying solely on international cards destroys conversions. The European Payments Council reports that the global average cart abandonment rate sits at an alarming 78%, with a primary cause being the absence of preferred local payment methods at checkout. Industry research highlights that adding just two preferred local payment options in a specific market can instantly boost checkout conversion rates by 10% to 30%. For instance, failing to offer the iDEAL payment method in the Netherlands can result in missing out on up to 60% of potential sales.

Intelligent Cross-Border Acquiring

Today's cutting-edge solutions differentiate themselves through intelligent cross-border acquiring. Instead of forcing merchants to establish local entities everywhere, top platforms leverage their own localized acquiring licenses.

-

Actionable Scenario: Imagine a global gaming platform expanding into Southeast Asia. Instead of opening entities in Indonesia, Malaysia, and Thailand independently, they integrate Antom as their regional acquirer. The gamer pays in local currency using local cards, ensuring an unprecedented 90%+ authorization rate. Meanwhile, Antom's Global FX Optimization API deposits funds directly into the merchant's master account in USD, bypassing massive FX markup fees.

Checklist for Auditing an Acquirer

Don't base your procurement decision solely on sales presentations. Ask these specific technical questions to determine whether a provider's acquiring services fit your operational needs:

-

Can you provide authorization rate benchmarks relevant to my industry and top three target countries? (If they only offer a "global average," they could be hiding weak regional performance.)

-

Do you hold local acquiring licenses in my expansion markets, or do you rely on third-party banking partners? (Direct local acquiring consistently yields faster settlement and higher approval rates.)

-

What is your rolling reserve policy for my MCC (Merchant Category Code)? (Always obtain written confirmation of maximum reserve caps.)

-

Do you support like-for-like settlement? (Central to cross-border acquiring: Can I charge my customers in Euros and receive Euros without being forced to pay an additional currency conversion fee?)

-

How detailed is your decline reason code reporting? (If a transaction fails, your tech team needs to know exactly why—e.g., "insufficient funds" vs. "do not honor"—so they can trigger the appropriate automated customer recovery email.)

By asking these questions, the conversation shifts away from "what is an acquirer" and toward "how will this acquirer enhance my unit economics."

Frequently Asked Questions About Merchant Acquiring

Q: In payments terminology, what is an acquirer vs. an issuer?

A: An acquirer and an issuer represent opposite sides of a transaction. The issuer is the bank that provides the consumer's credit card and approves the funds. The acquirer is your merchant bank that requests those funds and settles them into your business bank account.

Q: Do I always need a direct relationship with an acquirer?

A: No. Small businesses and early-stage startups often utilize Payment Facilitators (like Stripe) that aggregate many merchants under one master acquiring account. However, as transaction volumes reach the millions, direct acquiring services become essential for lowering interchange fees and maintaining control over risk thresholds.

Q: How does cross-border acquiring reduce FX fees?

A: Leading cross-border acquiring providers utilize local acquiring licenses to process transactions locally in the customer's native currency. This avoids costly cross-border interchange fees and opaque currency conversion markups typically imposed by traditional international processors.

Q: Why might an acquirer freeze my merchant account?

A: Acquirers bear the financial liability for your business. If they notice sudden, unexplained spikes in transaction volumes, a surge in chargebacks, or significant shifts in your business model that violate underwriting terms, they may freeze funds to cover potential refund liabilities.

Next Steps

Understanding what an acquirer does is only the starting point. In today's digital economy, the payment infrastructure you select determines your ceiling for global scalability. Generic payment processors may suffice for early-stage ventures, but for complex marketplaces, subscription models, or international e-commerce stores, relying on rudimentary solutions leads to hidden revenue leakage through false declines and poor FX management.

Do you need a financial partner equipped with adaptive risk engines and deep local banking relationships? Stop leaving money on the table. Elevate your authorization rates, streamline your compliance procedures, and confidently enter new markets with elite cross-border acquiring.

Consult with the Antom Solutions Architecture Team now to assess your current payment stack and develop an optimal global payout strategy.

About the Author: The Antom Global Payments Intelligence Team

This guide was compiled by Antom's Payment Intelligence Team—a group of certified B2B payment architects, compliance specialists, and risk mitigators with decades of combined experience in card network rules, merchant underwriting, cross-border settlement, and high-authorization transaction routing for enterprise platforms and global digital merchants.