Share on

Key Insights

- The United States, with only 5% of the global population, generates over 20% of the world’s total income, making it the largest single national economy globally. In 2025, the per capita GDP of the U.S. is projected to reach USD 89,599, ranking eighth globally.

- Offline retail in the U.S. currently remains mainstream, accounting for 84% (approximately USD 6.1 trillion) of the overall domestic retail market. The online share is only 16%, approximately USD 1.2 trillion. Large chain retailers (such as Walmart, Target, and Costco) dominate the market, with Walmart’s annual revenue exceeding USD 600 billion in 2024, firmly securing its leading position. Amazon, Apple, and Home Depot follow closely behind.

- The top 10% of highest-earning households in the U.S. account for over 50% of retail spending, indicating that middle-to-high-income households are the backbone of the market. Specifically, with respect to direct consumption by the affluent elderly aged 50 and above, 56 cents of every USD 1 spent in the U.S. comes from individuals aged 50 and above. They are the true “big spenders” of the U.S. consumer market.

- 90% of grocery consumers will choose omnichannel (online + offline) retail. The line between online and offline has long been blurred, and omnichannel operations have evolved from a “plus factor” to a “survival line”.

- 67% of the U.S. consumers have used BOPIS (Buy Online Pick-up In Store) services, and among them, 75% indicated they would likely continue to choose this shopping method in the future. In addition, 50% of consumers consider the availability of in-store pickup an important factor when choosing an online store.

- In the U.S., traditional bank cards still dominate, with credit and debit card payments collectively accounting for approximately 65% of the market share, making them the primary payment method for U.S. consumers, who hold an average of 3.9 credit cards per person. Card-linked wallets (33%) are used significantly more than non-card-linked wallets (8%).

- In the U.S. market, which is highly reliant on card payments, merchants face a significantly increased risk of fraud. With the application of AI technology, fraudulent activities will become even more covert and sophisticated.

- The door to the offline retail market in the U.S. is wide open, but competition based on cost-effectiveness, social e-commerce, AI applications, payment security, and supply chain restructuring—each link tests merchants’ adaptability. Only through refined operations and a comprehensive layout can one secure a foothold in this vast market with a total population of 340 million.

Foreword

5% of the Population, Yet Generating 20% of Global Income – Decoding the Underlying Logic of the U.S. Consumer Market

At the Apple Store on Fifth Avenue in New York, people are crowded around tables, jostling to see Apple’s latest iPhone 17. As the world’s largest consumer market, the U.S. accounts for only 5% of the global population but generates over 20% of the world’s total income. However, this seemingly prosperous market is undergoing an unseen transformation: tightening immigration policies are slowing labour force growth, the consumption gap between affluent elderly and young low-income families is widening, and the digital wave is reshaping the traditional retail landscape.

In 2024, total offline retail sales in the U.S. (including automotive and gasoline sales) reached USD 6.1 trillion, but the growth rate has returned to normal from the post-pandemic revenge spending. Retail giants such as Walmart, Target and Costco are deepening their competitive moats through omnichannel layouts, private labels and membership systems. Common foreign offline brands such as UNIQLO, H&M and Zara in fashion have physical stores in major U.S. cities, while home and lifestyle brand IKEA has large offline stores in multiple states across the U.S.

Supported by easing inflation, expectations of interest rate cuts by the Federal Reserve and tax reduction policies, the U.S. retail market is showing both resilience and divergence. Who can stand out amid the dual challenges of digital transformation and consumer stratification?

Overview of the U.S.

Overview of the U.S. Market

Buy, Buy, Buy! This is a typical adjective for U.S. consumption. The country’s private consumption robustly drives GDP growth at an annual rate of 2.6%, confirming that “consumer confidence” remains the core fuel of the economic engine.

The total population of the U.S. reached 335 million in 2024, with a median age of approximately 38.7 years. Nearly 65% are in the labour force, aged 15-64. The official language is English. Spanish is the most widely spoken language in the U.S. after English, making the U.S. the world’s second-largest Spanish-speaking country. The U.S. is also home to hundreds of other languages spoken by its residents, including but not limited to Mandarin, French, German, Hindi, Arabic, Vietnamese, Tagalog and Portuguese.

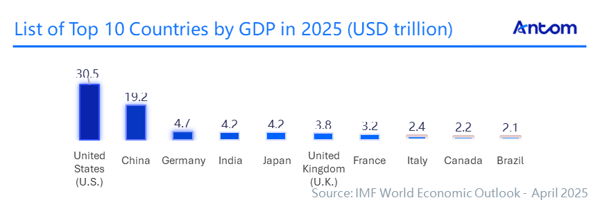

According to the International Monetary Fund (IMF)’s World Economic Outlook, which measures global economies by nominal GDP in USD, the U.S. will be the world’s largest economy in 2025 with a GDP of approximately USD 30.5 trillion, accounting for approximately 20% of global GDP. Other countries such as China, Germany, India, and Japan follow closely behind. In 2025, the per capita GDP of the U.S. is projected to reach USD 89,599, ranking eighth globally. These data indicate that American consumers have strong purchasing power and robust demand for high-quality goods and services.

Market estimates suggest that U.S. GDP growth will slow from 2.9% in 2023 to a projected 2.1% in 2025. GDP continued to grow in size, but at a slower pace than in 2023.

S&P’s sovereign credit rating for the U.S. is AA+/A-1+. The U.S. lost its AAA sovereign rating from S&P after the 2011 debt-ceiling crisis.

As of 25 November 2025, although the USD monetary market generally remained stable, it exhibited a “divergent” characteristic, showing differentiated trends against various currencies—a phased weakening against major developed country currencies, while continuing to maintain strength against emerging market and low-interest-rate currencies. It is also worth noting that the RMB has recently shown relative strength—breaking through the 7.09 mark on 25 November to reach a new high since November last year, indicating an appreciation trend of the RMB against the USD. This aligns with the divergent characteristics of the overall market performance of the USD, reflecting the differing relative performance of emerging market currencies during specific periods.