Share on

Mobile payment solutions allow customers to complete a transaction within seconds with just a tap or scan. This eliminates slow checkouts and increases payment options, thus improving consumers’ overall experience. In addition, mobile payments facilitate higher financial inclusion by allowing people with smartphones access to online commerce and financial services. As a global merchant, integrating mobile payment solutions into your payment system can improve conversions across international markets.

Global mobile payment solutions market analysis

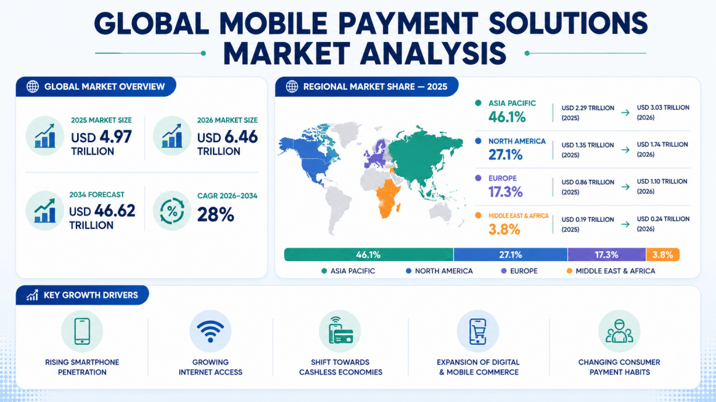

In 2025, the global market value of mobile payment solutions was USD 4.97 trillion. Projections show that this amount will grow to USD 6.46 trillion in 2026 and USD 46.62 trillion by 2034, growing at a compound annual growth rate (CAGR) of 28%. This market size will continue growing due to the increased penetration of smartphones, the internet, and the global shift towards cashless economies.

While the use of mobile payments is increasing globally, some regions have higher adoption than others. For instance, the Asia Pacific region dominated the market with a market share of 46.1% compared to Europe at 17.3%. These differences occur due to factors like mobile phone penetration, local payment habits, and financial infrastructure.

|

Region |

Market size |

|

Asia Pacific |

Dominates the global mobile payment market with a market share of 46.1% in 2025, accounting for USD 2.29 trillion. It will reach USD 3.03 trillion in 2026. |

|

North America |

North America has the second-largest market for mobile payment solutions, valued at USD 1.35 trillion (27.1% of the global market). It will reach USD 1.74 trillion in 2026. |

|

Europe |

In 2025, Europe represented 17.3% of the global mobile payments market, valued at USD 0.86 trillion. It will grow to USD 1.1 trillion by 2026. |

|

Middle East & Africa |

The Middle East & Africa market for mobile payment solutions is growing due to the increased penetration of mobile phones and high-speed internet. Its value in 2025 was USD 0.19 trillion (3.8% of global revenue) and will reach USD 0.24 trillion in 2026. |

What are mobile payment solutions?

Mobile payment solutions are technologies and payment methods that allow customers to complete transactions through smartphones, tablets, or other mobile devices. They support payments across mobile websites, apps, digital wallets, QR code-based systems, and other mobile-led checkout experiences. This means that customers do not have to rely on traditional desktop payment flows to complete transactions.

Mobile payment solutions support cross-border businesses by improving the payment experience for international customers. They help your business support faster checkout, reduce manual data entry, and align with mobile shopping habits in different markets.

Types of mobile payment solutions

Your cross-border payment system should support multiple mobile payment solutions depending on target customer behaviours and sales channels. For example, some regions may use mobile money apps more, while others use QR codes. Understanding these types of solutions can help you select localised options to improve the overall customer experience.

Mobile wallets

A mobile wallet is a digital app that customers download on their phones. It allows them to create accounts and save payment information, which they then use to make or receive payments with a few taps. Mobile wallets eliminate the need to carry debit or credit cards and cash, thus making the process more convenient.

The global market for mobile wallets was at USD 238.26 billion in 2025 and will grow to USD 784.67 billion by 2032, reflecting a CAGR of 18.56%. Examples of these mobile wallets include WeChat Pay, Apple Pay, Google Pay, PayPal, and Cash App. Incorporating these payment options increases your customers’ payment options, potentially reducing cases of cart abandonment.

QR code payments

QR code payments allow customers to scan a code to complete a transaction. Industry data shows that the global adoption of this payment method continues to grow significantly as more people embrace mobile solutions. For example, Juniper Research shows that the value of QR code payment transactions will increase from USD 5.4 trillion in 2025 to USD 8 trillion by 2029. This reflects a 48% growth rate between 2025 and 2029.

As a global merchant, integrating QR code payments into your system can help you leverage this global opportunity and improve your brand’s appeal to tech-savvy customers. Besides, the accessibility and affordability of the QR code infrastructure compared to traditional point-of-sale technology lower the barrier to entry.

In-app payments

If your business has a mobile app, you can add an integrated payment method that allows customers to complete transactions without leaving the app. For example, they can store card information or a digital wallet to enable them to check out without constantly entering their payment information every time they buy from you. This can create a more seamless experience by removing the need to redirect users to external payment pages.

In 2025, about 3.8 billion smartphone users used applications that included some form of in-app purchasing. During this period, the value of the in-app purchase market was USD 247.6 billion, which will continue to grow at a CAGR of 12.6% to reach USD 721.4 billion by 2036. This growth indicates the potential of in-app payment solutions in helping businesses capture more sales through app-based commerce.

Direct carrier billing and other mobile-led options

Direct carrier billing is a mobile payment solution that allows customers to charge purchases or subscriptions directly to their monthly phone bill or deduct from their prepaid balance. This option is particularly ideal for digital goods, subscriptions, and selected mobile-first services. Projections show that between 2026 and 2030, the global value of direct carrier billing transactions will increase from USD 51 billion to USD 87 billion. The key areas contributing to this growth will include digital ticketing and physical goods.

Other mobile-led payment options may include app-based bank transfers, one-click wallet payments, or region-specific mobile checkout methods designed to simplify transactions on smartphones.

How mobile payment solutions boost cross-border sales

Mobile payments can influence how quickly customers complete a purchase, how comfortable they feel using your checkout, and how easily they return to buy again. For example, customers may keep coming back to your business if you allow localised mobile wallets because they eliminate the burden of carrying physical cards and cash everywhere.

But how do these solutions contribute to your sales?

Supports mobile-first shopping behaviours

In many markets, customers rely on smartphones as their main shopping device. For instance, 48% of global shoppers used a smartphone to make their latest purchase, whether online or in-store. In addition, 32% perform digital window shopping with a mobile device daily, while another 32% use their mobile phones to browse merchant sites.

Most of these consumers browse products, compare prices, and complete purchases through apps and mobile websites rather than desktop platforms. Mobile payment solutions help your business meet these expectations by making it easier for customers to pay in ways that suit mobile-first shopping habits.

Improves checkout speed and convenience

Typing card details, billing information, and verification codes on a smartphone can slow down the checkout process. Mobile payment solutions simplify this journey by supporting saved credentials, one-tap checkout, or wallet-based payments that reduce the amount of manual input required. On average, these digital wallets can reduce the checkout time by half. This improvement boosts sales by making the payment experience faster and more convenient for international customers.

Reduces cart abandonment on mobile

Nearly 70% of online shoppers leave their cart without completing the purchase, leading to a USD 4.6 trillion loss in annual sales. Mobile payment solutions address this challenge by making the payment process easier for buyers. For instance, Google Pay and Apple Pay reduce cart abandonment rate by 18% compared to manual entries. This shows that streamlining checkout and reducing friction on smaller screens with mobile payment solutions can increase your sales.

Supports omnichannel and in-app commerce

Cross-border sales do not always begin and end on the same channel. A customer might discover a product through a mobile app, continue browsing on a mobile website, and complete the purchase later through another digital touchpoint. Mobile payment solutions can help support a more connected payment experience across apps, mobile sites, and other digital channels, while also enabling smoother in-app transactions.

For example, platforms like Antom allow you to support mobile wallets, in-app payments, and other local mobile payment experiences across global markets through a single integration. This one-stop solution allows you to launch your business in more than 200 markets worldwide, select from over 300 payment methods and 140 currencies. This diversity allows you to manage cross-border payments while creating more localised checkout experiences for international customers.

Final takeaway

Mobile payment solutions allow you to take advantage of the ongoing shift towards cashless economies. With localised mobile wallets, you can allow your customers to use familiar payment solutions to complete their online purchases. This can help build trust and reduce cart abandonment, thus boosting cross-border sales.

Planning to expand into mobile-first markets? Discover how Antom can help you achieve that goal.

FAQs

1. Can mobile payment solutions support both domestic and cross-border transactions?

Yes. Many mobile payment solutions can support both domestic and international transactions, although the payment methods available may vary by market. This can help businesses create a more consistent mobile payment experience while still adapting to local customer preferences.

2. Are mobile payment solutions relevant for B2B businesses?

They can be, especially if your business sells through mobile websites, apps, or digital platforms used by business buyers. While B2B payment journeys may differ from consumer transactions, mobile payment solutions can still support faster checkout, easier repeat purchases, and more convenient payment experiences for customers using mobile devices.