Share on

Cross-border Payouts Explained: Methods, Costs, Challenges, and How to Optimize Global Payments

Cross-border payouts are a core part of how modern businesses operate globally. As companies expand across markets, they increasingly need to send funds to individuals and businesses in different countries, often in multiple currencies and through different payment systems.

However, behind what looks like a simple “send money” action lies a complex infrastructure involving currency conversion, payment networks, compliance checks, and routing decisions. These layers directly impact payout speed, cost, and success rate.

This guide explains what cross-border payouts are, how they work, the main payout methods, key cost drivers, common challenges, and how businesses can optimize payout performance at scale.

Why cross-border payouts matter for global businesses

In today’s global economy, businesses no longer operate within a single market. Platforms hire international talent, marketplaces onboard global sellers, and digital companies serve customers across multiple regions.

While collecting money globally is relatively mature, sending money globally (cross-border payouts) remains fragmented and complex.

Slow settlement times, FX volatility, and fragmented banking systems often create hidden operational friction. For scaling businesses, payout performance directly impacts seller retention, freelancer satisfaction, and overall market expansion.

Modern payment infrastructure is therefore shifting from simple transaction processing to global payout orchestration, enabling businesses to move money faster, more transparently, and at lower cost.

What are cross-border payouts?

Cross-border payouts are business-initiated outbound payments sent from one country to recipients in another country, often involving currency conversion and multiple payment networks.

These recipients may include:

- Marketplace sellers

- Freelancers and contractors

- Suppliers and vendors

- Creators and affiliates

- Customers receiving refunds or claims

Unlike domestic payments, cross-border payouts must coordinate across multiple financial systems, regulatory environments, and currency networks.

Cross-border payments vs. cross-border payouts: What’s the difference?

Although often used interchangeably, the two concepts differ:

- Cross-border payments refer to any transaction between two parties in different countries (including consumer payments).

- Cross-border payouts specifically refer to business-initiated outbound payments to global recipients.

In short:

All cross-border payouts are cross-border payments, but not all cross-border payments are payouts.

The key distinction lies in direction and purpose—payouts are typically operational disbursements tied to business activities such as revenue sharing, salaries, or marketplace settlements.

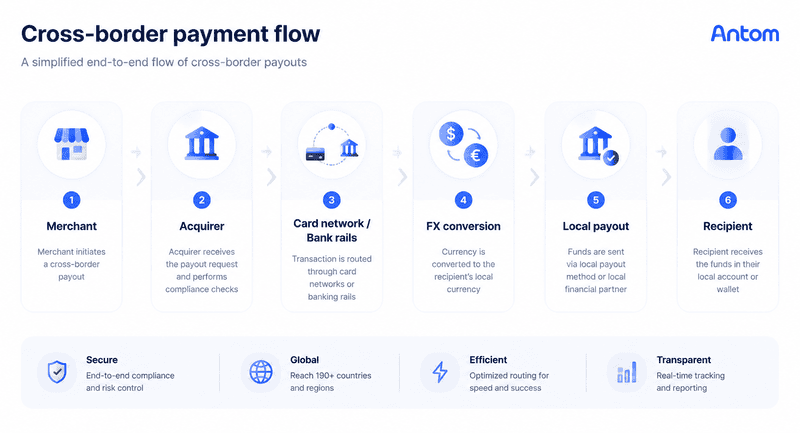

How do cross-border payouts work?

Cross-border payouts involve multiple infrastructure layers working together:

Payout initiation

A business initiates a payout through an API, dashboard, or batch file. This can involve single or mass payouts.

Recipient and compliance validation

Recipient identity, banking details, and regulatory requirements are verified. This ensures compliance with local AML and financial regulations.

FX conversion

If currencies differ, funds are converted using FX rates. This stage often introduces FX spreads and hidden payment costs depending on provider transparency.

Routing across payment rails

Payments are routed dynamically across:

- Bank networks (SWIFT)

- Card networks (Visa, Mastercard)

- Wallet ecosystems

- Local real-time payment systems

Settlement and reconciliation

Funds are delivered to the recipient, followed by reporting, tracking, and reconciliation across systems.

Common cross-border payout use cases

Cross-border payouts support a wide range of global business models, especially platforms and companies operating across multiple countries and currencies. These use cases are typically driven by revenue distribution, service compensation, or financial settlement between businesses and individuals. Below are the most common payout scenarios in global payment infrastructure.

Cross-border payout use cases overview

|

Use case |

Description |

Example |

|

Marketplace seller payouts |

Platforms distribute earnings to global sellers based on sales and revenue sharing |

An e-commerce platform paying sellers in multiple countries after order completion |

|

Freelancer and contractor payouts |

Gig economy platforms pay remote workers across borders |

A global platform paying designers or developers in different regions |

|

Creator and affiliate payouts |

Digital platforms distribute commissions and monetization revenue |

A content platform paying influencers or affiliate marketers |

|

Supplier and vendor payments |

Businesses settle cross-border procurement and trade invoices |

A company paying overseas suppliers for goods or services |

|

Customer refunds and claims payouts |

Businesses issue cross-border refunds or compensation |

An e-commerce refund or insurance claim payout to international customers |

Main cross-border payout methods

In global payout operations, no single payment method works for every market or use case. Businesses typically rely on a combination of different payout rails depending on factors such as speed, cost, coverage, and regulatory requirements.

Bank transfers and SWIFT

Traditional method with wide coverage but slower settlement and higher intermediary bank fees.

Card-based payouts

Visa Direct and Mastercard Send enable near real-time payouts to debit cards.

Digital wallets and mobile money

Wallet ecosystems like DANA, AlipayHK, and regional mobile money systems enable fast local disbursements.

Local real-time payment rails

Systems like UPI, Pix, SEPA Instant enable low-cost instant domestic settlement, increasingly used for cross-border flows via local partners.

Multi-rail payout platforms

Modern payment infrastructure platforms unify multiple rails through a single API, enabling intelligent routing and optimization.

Cross-border payout fees and hidden costs

Cross-border payout costs extend beyond visible transaction fees and should be understood as a layered cost stack:

|

Cost Layer |

Description |

|

Transaction fees |

Direct per-transaction processing fees |

|

FX spreads |

Difference between market and applied FX rates |

|

Intermediary bank fees |

Fees from correspondent banking networks |

|

Receiving fees |

Charges applied by recipient banks |

|

Compliance costs |

|

|

Operational costs |

Manual reconciliation, support, engineering overhead |

|

Integration costs |

Maintaining multiple payout connections |

True cost is determined by cumulative infrastructure inefficiencies, not a single fee.

Example: $10,000 cross-border payout (US → Brazil)

To understand how hidden costs impact global payouts, let’s take a realistic example of a marketplace platform paying a seller $10,000 from the US to Brazil.

At first glance, the transaction seems simple. However, once all layers of the payout infrastructure are included, the actual cost structure becomes significantly more expensive.

Transaction fee

The payout provider charges:

- 1.2% per transaction

= $120

FX spread

Market FX rate: 1 USD = 5.00 BRL

Provider applied rate: 1 USD = 4.85 BRL

Hidden FX loss: ~3%

- $10,000 × 3% = $300

Intermediary bank fees (SWIFT routing)

- Correspondent banks charge multiple hops

- Typical fee: $10–$25 per bank × 2–3 banks

Estimated total: $60

Receiving bank fee (Brazil local bank)

- Incoming international transfer fee

= $40

Compliance & screening cost (internal + provider overhead)

Includes:

- AML checks

- sanctions screening

- transaction monitoring

Allocated cost per payout (scaled average):

= $30

Operational & reconciliation cost

Includes:

- failed payout handling

- finance team reconciliation

- support tickets

- engineering maintenance across rails

Estimated per transaction cost:

= $80

Total real cost breakdown

|

Cost component |

Amount |

|

Transaction fee |

$120 |

|

FX spread loss |

$300 |

|

Intermediary bank fees |

$60 |

|

Receiving fee |

$40 |

|

Compliance cost |

$30 |

|

Operational cost |

$80 |

|

Total hidden + visible cost |

$630 |

On a $10,000 payout, the business loses: $630 (6.3% total cost)

But more importantly:

- The seller receives less than expected

- Finance teams spend time reconciling issues

- Support teams handle disputes

- Scaling to thousands of payouts multiplies this cost dramatically

Why this matters for global businesses?

Cross-border payout costs are not just “fees”—they are a profit leakage system.

At scale:

- 10,000 payouts/month → $75.6M annual leakage

- Plus operational drag and slower expansion

- Plus reduced seller satisfaction and retention

What looks like a simple $10,000 transfer is actually a multi-layer cost stack involving FX, networks, compliance, and operations, making cross-border payouts one of the most underestimated cost centers in global commerce.

Why cross-border payouts fail

Common failure points include:

Incorrect recipient data

Invalid account numbers, wallet IDs, or routing information.

Currency mismatch

Unsupported or incorrectly configured currency pairs.

Compliance rejection

Regulatory or sanctions-based transaction blocking.

Unsupported payment rails

Destination country does not support selected payout method.

Routing and intermediary issues

Failures caused by fragmented banking networks or poor routing paths.

For example, a subscription business in Singapore may experience involuntary churn when cross-border recurring payments fail due to expired cards, insufficient balance at billing time, or issuer-side authorization issues, even though the customer did not intend to cancel.

This is not just a payment failure issue, but a form of revenue leakage caused by infrastructure-level friction in cross-border payout systems.

Key challenges in cross-border payouts

Slow settlement times

Payments may take days due to correspondent banking delays.

High and unpredictable costs

FX spreads and hidden fees reduce cost transparency.

Regulatory complexity

Each market introduces different compliance requirements.

Limited payment visibility

Lack of real-time tracking and reporting across providers.

Multi-provider complexity

Businesses must manage multiple integrations across regions.

Manual reconciliation

Finance teams often rely on spreadsheets for payout matching.

How to optimize cross-border payouts

Use local payment rails where possible

Reduce cost and improve settlement speed by leveraging domestic infrastructure.

Choose multi-rail routing

Route payments dynamically across bank, card, wallet, and RTP networks.

Improve FX transparency

Use real-time FX rates and reduce hidden spreads.

Automate recipient validation

Reduce payout failures through pre-checks and structured data validation.

Centralize reporting and reconciliation

Unify payout data across markets for better financial visibility.

Use smart routing to improve success rates

Optimize payout paths based on cost, speed, and reliability signals.

How to choose a cross-border payout provider

Businesses should evaluate providers based on:

- Geographic coverage

- Supported currencies

- Available payout rails

- FX transparency

- Payment success rate

- API and integration simplicity

- Compliance and licensing coverage

- Reporting and reconciliation capabilities

- Scalability across markets

Decision quality determines long-term payout efficiency.

How Antom helps businesses optimize cross-border payouts

Antom provides a unified global payment infrastructure designed to simplify cross-border payout operations.

With a single integration, businesses can access multiple payout rails, currencies, and settlement methods while maintaining control over cost, speed, and visibility.

Key capabilities include:

- Multi-rail payout support across global markets

- Smart routing to optimize cost and success rates

- Multi-currency payout infrastructure

- Unified reporting and reconciliation layer

- Scalable API integration for global expansion

By reducing fragmentation across payment systems, Antom enables businesses to transform payouts from an operational burden into a scalable infrastructure advantage.

FAQs

What are the main payout methods?

Bank transfers, card networks, wallets, and local real-time payment systems.

Why are cross-border payouts expensive?

Due to FX spreads, intermediary fees, compliance costs, and operational inefficiencies.

How can businesses optimize payouts?

By using local rails, smart routing, FX transparency, and unified payment infrastructure.

Conclusion

Cross-border payouts are no longer a simple financial function—they are a core component of global business infrastructure.

As businesses expand internationally, payout performance directly affects liquidity, partner satisfaction, and market scalability. Companies that optimize payout infrastructure gain a significant competitive advantage in global markets.

Modern payment infrastructure, built on multi-rail connectivity, smart routing, and unified APIs, is transforming payouts from a cost center into a growth enabler.