Share on

Independent stores encounter their own set of obstacles at checkout. Generating traffic to an e-commerce website takes work. Losing customers at checkout is another matter entirely. Low authorization rates and sudden chargebacks threaten profits in ways they cannot see or sense.

Choose your global payment platform carefully. Its effect can have a direct bearing on the success of your checkout numbers. Modern buyers actively look for frictionless experiences. To build a store with high success, an effective strategy must be in place. This involves developing a robust payment platform that goes beyond standard credit card offerings. It must meet global consumer habits as well as quickly evolving consumer patterns.

1. Independent Stores' Payment Dilemma: Why They Lose Sales at Checkout

1.1 Cart Abandonment

Cross-border e-commerce is growing at an incredible rate. A report by Juniper Research shows this clearly. Global cross-border e-commerce transactions will surpass $3.3 trillion by 2028. This represents an astonishing 107% growth since 2023!

Yet many independent sellers fail to fully capitalize on this growth. High cart abandonment rates remain a serious obstacle. According to industry data provided by the European Payments Council, the average global cart abandonment rate is 78%. For cross-border shopping, cart abandonment can reach as high as 90%!

Merchants' failure to offer payment methods that meet local preferences is the primary source of frustration among top global markets. This leads to an unpleasant checkout experience for shoppers. Your payment platform must help bridge this gap.

1.2 Credit Cards Versus Local Payments: Finding an Appropriate Solution

Credit cards remain immensely popular across North America. Yet certain markets rely heavily on alternative payment networks. These channels may not be supported by your standard platform.

European shoppers tend to favor bank transfers for purchases. Local services like Klarna are popular choices in Europe. On the other hand, shoppers in Southeast Asia and Latin America tend to rely more on mobile digital wallets like DANA or Pix for real-time transactions.

Your international payment platform could be leaving money on the table. Only accepting major credit cards limits your revenue. To maximize conversions and build global buyer trust, a flexible platform that offers various payment choices to meet global customer requirements should be utilized.

2. Increase Conversions With A Two-Pronged Checkout Strategy

2.1 Strategy 1: Optimizing Credit Card Acceptance Rates

Credit cards remain the cornerstone of global commerce. Yet international transactions often lead issuing banks to implement "soft declines". In order to protect your revenue, it is crucial that you select an international payment platform with optimal acceptance rates. This benchmark should ideally exceed 95%, as stated by Antom Knowledge.

When your payment platform acceptance rate drops below 88%, profit losses become substantial. Conversely, acceptance rates exceeding 98% could indicate weak fraud filters. This flaw opens up costly credit card scams.

2.2 Strategy 2: Integrating High-Converting Local Wallets

Antom Knowledge data shows that localized alternatives are highly effective at recovering lost sales. They quickly adapt and become cost-cutting measures. Simply offering two local payment options can boost your conversion rates by 10% to 30%. By forgoing popular payment systems such as iDEAL in the Netherlands, for instance, you risk missing up to 60% of potential sales opportunities!

An effective global payment platform must integrate these local alternative payment methods (APMs) seamlessly. It should automatically provide buyers with the most suitable payment option based on their location. In addition, secure platforms should feature advanced chargeback control mechanisms and modern risk management tools for maximum safety and protection.

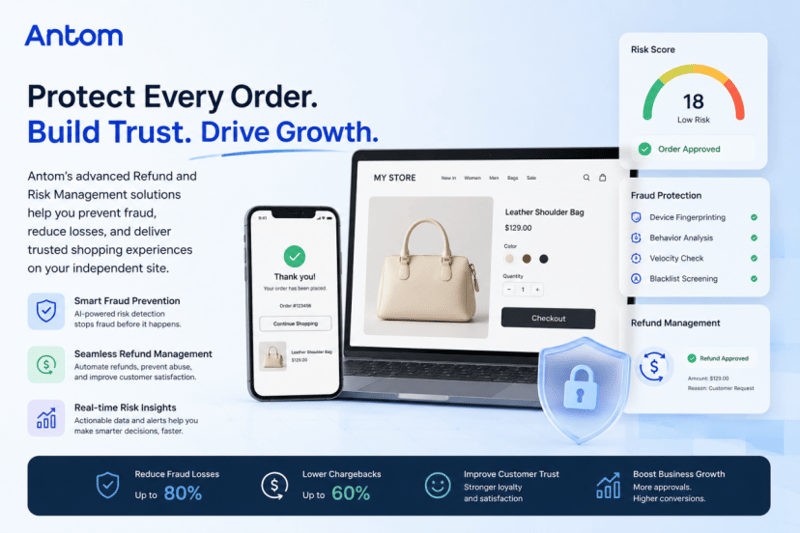

3. Protect against Fraud Through Advanced Chargeback and Risk Management Solutions

3.1 Understand Friendly Fraud and Declines

Independent sellers are frequently targeted by fraudsters. They suffer chargeback or card-testing attacks. Traditional fraud filters rely on outdated systems and rigid rules. They provide protection from theft while potentially interfering with legitimate sales. This phenomenon is known as "friendly fraud". It leads to false positives that cause legitimate sales to suffer.

3.2 Utilizing AI Smart Routing and Auto-Retry Mechanisms

To prevent such incidents from taking place, your overseas payment platform must utilise cutting-edge technology. Today's cross-border platforms use AI-powered smart routing as a solution for checkout friction. Antom Product Docs indicates that their payment orchestration platform utilizes AI algorithms for real-time assessment of transactions. Should soft declines be detected, smart retries will automatically occur. Otherwise, matching orders with local acquirers happens instantly.

This adaptive payment platform technology has the capacity to recover up to 15% of lost revenue. It minimizes false risk triggers while simultaneously stopping real fraud. This keeps checkout lanes open for honest customers.

4. Checklist to Identify an Appropriate Payment Partner

- Transparent Fees: Avoid hidden margins. According to research by Fortune Business Insights, traditional international transfers still carry an average cost of 6.35% due to higher foreign exchange margins. To lower this burden, seek an efficient payment platform with transparent pricing.

- Peak Stability: Keep reliable uptime during holiday peaks like Black Friday. Any minute of downtime could have serious repercussions for businesses. An analysis by Antom Knowledge highlights this critical need. Payment platforms must maintain an outstanding 99.99% uptime record to remain successful.

- Unified API Integration: Streamline manual integrations for each country. Consider an advanced payment platform with an automated payment orchestration layer. One API connection provides instantaneous access to hundreds of global payment options.

5. FAQs (Frequently Asked Questions)

Q: How can I reduce failed payments on my independent store?

A: For best results, a modern payment platform equipped with AI-driven smart routing and auto-retry logic will prove beneficial. This enables transactions to seamlessly reroute back to alternative local acquiring banks should their initial attempt at payment fail.

Q: What is an acceptable payment acceptance rate for cross-border e-commerce?

A: When selecting your payment platform, ensure it has an authorization rate of 95%. This maximizes sales while protecting against chargeback penalties and fraud.

Q: Will using multiple local payment methods cause my checkout page to load slowly?

A: Not necessarily when using an integrated payment platform supported by a payment orchestration provider. These systems use one API. They dynamically display only payment options that correspond with each buyer's country, keeping checkout fast, smooth, and highly tailored.