Share on

For global businesses, payment expansion is not only about accepting cards in another currency. A scalable cross-border payment API should help teams support local payment methods, multiple currencies, payment status notifications, risk controls, settlement records, and reconciliation across markets.

That makes cross-border payment API integration both a technical project and a business infrastructure decision. Developers need reliable APIs and test environments. Product teams need a localized checkout experience. Risk teams need fraud controls and authentication logic. Finance teams need clear reporting, settlement, and reconciliation workflows.

This guide is designed for developers, product managers, payment operations teams, finance leaders, and global expansion teams preparing to launch or consolidate payment infrastructure across multiple countries and regions.

Use this checklist to plan what to prepare before development, what to test before going live, and how to evaluate whether a cross-border payments API can support long-term international growth.

What Is Cross-Border Payment API Integration?

Cross-border payment API integration is the process of connecting a business website, app, platform, or backend system with payment infrastructure that can process international transactions across countries, currencies, payment methods, and settlement requirements.

A typical integration allows your system to:

-

Create payment requests from a merchant server or platform backend

-

Present relevant local payment methods to customers at checkout

-

Process cards, digital wallets, bank transfers, online banking, QR-based payments, or other local payment options

-

Receive real-time or asynchronous payment status updates

-

Handle refunds, cancellations, disputes, and failed transactions

-

Support transaction reporting, settlement tracking, and reconciliation workflows

For a domestic checkout flow, a business may only need a local payment gateway or card processor. For cross-border commerce, the requirements are broader. Customers may expect familiar local wallets in one market, online banking in another, cards in another, and market-specific authentication or risk checks across all of them.

That is why cross-border payment API integration should not be treated as a single checkout feature. It should be planned as a payment infrastructure layer that connects customer experience, backend logic, payment operations, risk control, and finance workflows.

When Does a Business Need a Cross-Border Payments API?

A business should consider a cross-border payments API when it plans to sell across multiple countries or regions and wants to support localized payment acceptance without rebuilding payment infrastructure market by market.

Common use cases include:

-

Ecommerce brands selling internationally

-

Travel, airline, hotel, ticketing, and mobility platforms

-

Gaming, streaming, and digital entertainment companies

-

SaaS and subscription businesses

-

Marketplaces with buyers and sellers in different regions

-

Online education platforms and digital service providers

-

Apps selling digital goods, memberships, or premium services

-

Enterprises consolidating fragmented local payment integrations

If your team is already managing multiple payment providers, separate regional integrations, manual reconciliation, inconsistent checkout performance, or fragmented reporting across markets, it may be time to move toward a more unified cross-border payment API strategy.

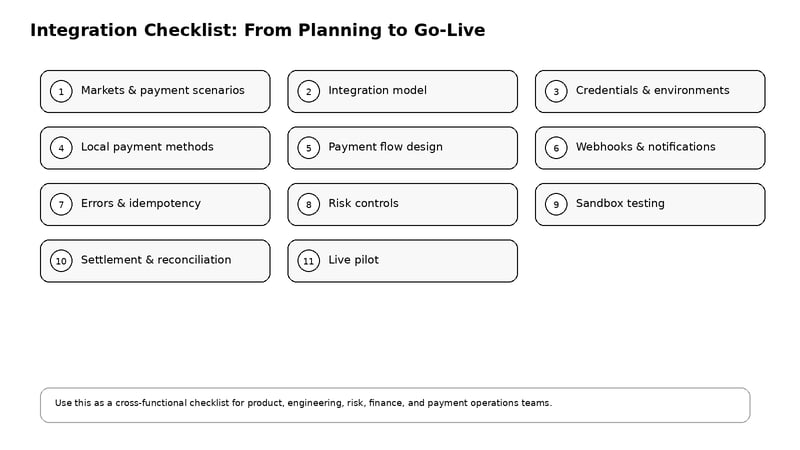

Cross-Border Payment API Integration Checklist

1. Define Your Target Markets and Payment Scenarios

Before choosing an API or writing code, define exactly where, how, and why customers will pay. This step prevents teams from building a payment flow around internal assumptions instead of real market behavior.

Your team should clarify:

-

Which countries or regions you want to support first

-

Which currencies customers will pay in and which currencies you want to settle in

-

Whether you need one-time payments, tokenized payments, subscriptions, or recurring billing

-

Whether your business model involves marketplace payouts, split payments, or vendor settlement

-

Which customer segments are most important in each market

-

Which payment methods local customers already trust

-

Whether refunds, partial refunds, cancellations, disputes, or chargebacks must be supported from day one

For example, a checkout experience designed around international cards may work in some markets but underperform where customers prefer digital wallets, online banking, QR-based payments, or local account-to-account transfers.

2. Choose the Right Integration Model

Not every business needs the same level of payment integration. A startup launching a new ecommerce store may prefer a hosted checkout or plugin-based integration. A larger platform may need API-level control over payment creation, checkout routing, user experience, reconciliation, and internal order states.

Common integration models include:

-

Hosted checkout page: A provider-hosted payment page that can reduce development effort and speed up launch.

-

Payment SDK: A software development kit that helps teams embed payment experiences into web or mobile apps.

-

Direct API integration: A more flexible option for teams that need deeper backend control and custom payment logic.

-

Ecommerce plugin: A faster path for businesses using common commerce platforms.

-

Payment orchestration layer: A setup for routing, managing, and optimizing multiple payment providers, gateways, acquirers, or payment methods.

-

Hybrid integration: A combination of checkout, SDKs, plugins, and APIs depending on region, product, or use case.

Hosted checkout can reduce development complexity. Direct API integration gives teams more control over the checkout and backend logic. Payment orchestration may be more suitable when a business needs to connect multiple gateways, acquirers, or local payment methods through one operational layer.

Antom supports flexible integration options for global businesses, including unified payment APIs, a pre-built checkout experience, developer documentation, sandbox tools, and payment orchestration capabilities. For teams comparing technical options, reviewing the Antom integration guide is a practical starting point before implementation.

3. Prepare API Credentials, Keys, and Environments

A reliable payment integration starts with environment setup. Development, staging, sandbox, and production resources should be clearly separated before code moves into a live environment.

At minimum, your development team should prepare:

-

Sandbox environment access

-

Production environment access

-

Gateway URL

-

Client ID

-

API keys

-

Public and private key handling

-

Signature generation and verification logic

-

Notification URL for payment status updates

-

Role-based access permissions for developers, operators, and finance users

Sandbox and live credentials should never be mixed. Do not reuse test keys in production, and do not store private keys in frontend code, shared documents, browser storage, or unsecured internal tools.

For Antom integrations, developers can configure sandbox resources, obtain client IDs and keys, set notification URLs, test payment behavior, and replace sandbox resources with live resources when moving to production. The Antom API reference and sandbox documentation can support this planning process.

4. Map Local Payment Methods by Market

Cross-border payment performance depends heavily on local payment method coverage. Before launch, create a market-by-market payment method map.

For each country or region, identify:

-

Common card networks and card authentication requirements

-

Popular digital wallets

-

Online banking methods

-

Bank transfer or account-to-account payment options

-

Buy Now, Pay Later options where relevant

-

Local payment method availability on mobile and desktop

-

Expected customer behavior for refunds, cancellations, and pending payments

This matters because customers often trust familiar payment methods more than a generic card form. In some markets, a local wallet or bank-based method may convert better than an international card option.

Antom provides access to a broad network of global and local payment methods through one integration. For businesses expanding across Asia and other high-growth markets, local payment method coverage should be part of the integration decision from the beginning. Teams can review Antom online payments documentation when mapping payment methods by market.

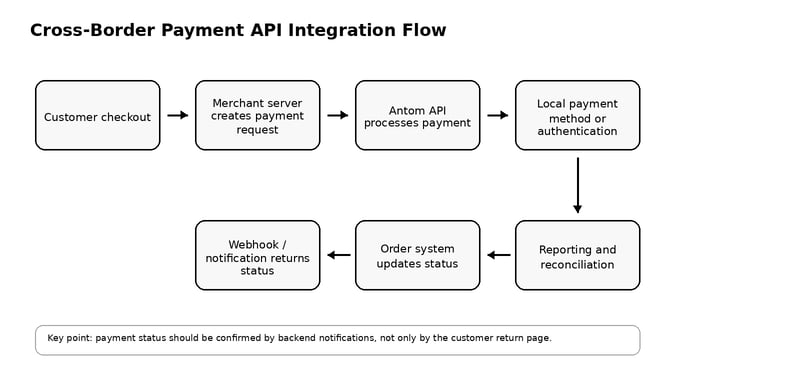

5. Design the Payment Flow Before Development

A cross-border payment API integration should be mapped as an end-to-end business flow, not just an API call. The flow should show how the customer, merchant backend, payment platform, risk checks, notifications, order system, and finance records work together.

A simplified payment flow may look like this:

The key is to define how your system handles every possible payment state, not only successful payments.

Questions to answer before development include:

-

What happens if a payment is pending?

-

When should an order be confirmed?

-

How long should the system wait before marking a payment failed?

-

What happens if the customer closes the browser before returning to the merchant site?

-

What if the webhook says success but the frontend return page does not load?

-

How are duplicate payment requests prevented?

For cross-border payments, asynchronous updates are especially important because some local payment methods do not behave like instant card authorizations.

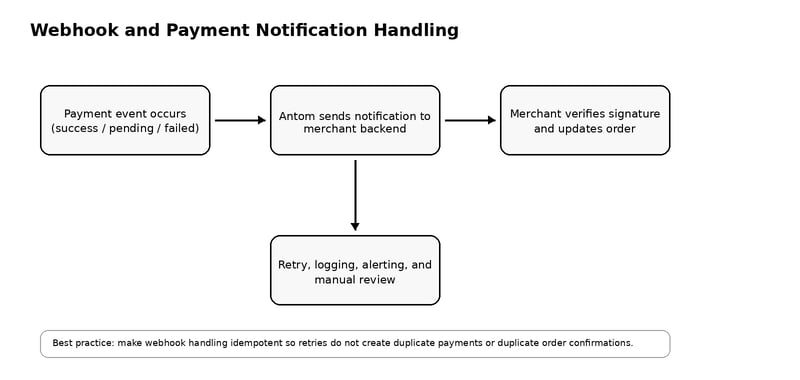

6. Set Up Webhooks and Payment Notifications

Webhooks are essential for payment reliability. A customer return page can be interrupted by browser issues, app switching, network failure, or user behavior. Your backend should not depend only on the customer being redirected back to your website.

Instead, your system should use payment notifications to update order status based on payment events sent to your backend.

Your webhook checklist should include:

-

A secure notification URL

-

Signature verification

-

Idempotent event handling

-

Retry logic

-

Event logging

-

Alerting for failed notifications

-

Mapping between payment status and order status

-

Manual review flow for unresolved cases

Antom integrations include notification URL configuration so merchants can receive payment notifications. This is especially important when supporting payment methods where the final payment status may be confirmed asynchronously.

7. Build for Errors, Retries, and Idempotency

Payment APIs operate in real-world conditions. Networks fail. Customers retry payments. Banks decline transactions. Wallet sessions expire. Providers return pending statuses. Internal services time out.

A strong integration should define how to handle:

-

Duplicate payment requests

-

Timeout responses

-

Pending payments

-

Failed payments

-

Customer cancellation

-

Invalid request parameters

-

Expired payment sessions

-

Refund failures

-

Dispute or chargeback events

Idempotency is especially important. If your backend retries a request after a timeout, the system should avoid accidentally creating duplicate payments or duplicate order confirmations.

Developers should also log request IDs, payment IDs, payment request IDs, timestamps, status codes, and provider response messages in a way that support, finance, and engineering teams can search later.

8. Add Risk Controls and Authentication

Cross-border payments carry different risk patterns from domestic payments. A business may face unfamiliar issuing banks, regional fraud patterns, account takeover attempts, unusual transaction velocity, refund abuse, or market-specific compliance requirements.

Your risk checklist should cover:

-

3D Secure or other authentication flows where applicable

-

Fraud screening rules

-

High-risk country or region handling

-

Device, behavioral, and transaction signals

-

Velocity checks

-

Refund abuse monitoring

-

Manual review thresholds

-

Dispute management workflows

Risk control should not be bolted on after launch. It should be part of the payment flow design because authentication, fraud screening, and checkout conversion are closely connected.

Antom provides risk management capabilities through Antom Shield, designed to help businesses monitor and protect online transactions. For global merchants entering new markets, this can be especially relevant when internal teams do not yet have enough local payment risk history.

9. Test in Sandbox Before Going Live

Sandbox testing should cover more than a single successful payment. A production-ready test plan should include both happy paths and failure paths.

A complete sandbox test plan should include:

-

Successful payment

-

Failed payment

-

Pending payment

-

Customer cancellation

-

Expired payment session

-

Refund and partial refund

-

Duplicate request

-

Invalid signature

-

Webhook retry

-

Browser return failure

-

Mobile checkout behavior

-

Local payment method behavior

-

Error message display

-

Order status update

-

Reconciliation record matching

Antom sandbox resources help developers validate payment behavior, integration resources, request and notification handling, and sandbox-to-live readiness before real customer traffic begins.

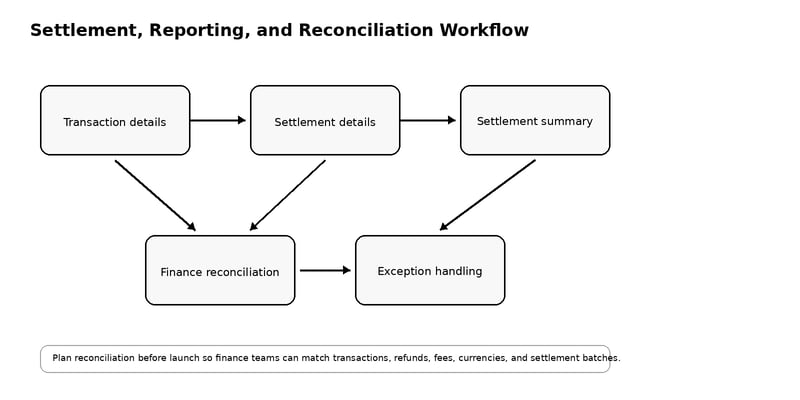

10. Plan Settlement, Reporting, and Reconciliation

Many payment integrations focus too much on checkout and too little on finance operations. That can create serious problems after launch, especially when markets, payment methods, currencies, refunds, settlement cycles, and fees become more complex.

Before launch, your team should answer:

-

How will transaction records be exported?

-

How will payment status be matched to order status?

-

How will refunds be reconciled?

-

How will settlement records be reviewed?

-

Which team owns payment exception handling?

-

What happens when transaction amount, settlement amount, fees, or currencies do not match internal expectations?

-

Does finance need dashboard access, API access, SFTP reports, or all of the above?

A good cross-border payment integration should help finance teams understand not only whether a payment succeeded, but how funds, fees, refunds, settlement details, and reconciliation records are handled.

Antom provides reconciliation reports, including transaction details, settlement details, and settlement summary reports that can support finance and operations workflows. For businesses operating at scale, reconciliation should be evaluated before launch, not treated as a post-launch detail.

11. Move to Live Mode Carefully

Going live should be treated as a controlled release, not a simple switch from test keys to production keys.

Before production launch, confirm that:

-

Merchant account activation is complete

-

Live client ID and keys are configured

-

Sandbox credentials have been removed from production code

-

Notification URL is set for the live environment

-

Webhook verification works in production

-

Payment method settings are enabled

-

Monitoring and alerting are active

-

Support teams know how to review payment issues

-

Finance teams know where to access reports

-

Pilot testing has been completed

Start with limited live testing before opening the integration to all users. This helps catch environment-specific issues that may not appear in sandbox, such as domain configuration, payment method availability, risk behavior, or notification delivery.

For Antom integrations, the go-live process includes replacing sandbox resources with live integration resources, configuring the live notification URL, and validating payment behavior in the live environment before scaling traffic.

Need help planning a multi-market payment integration?

Antom can help businesses evaluate local payment method coverage, integration models, risk controls, reporting requirements, reconciliation workflows, and go-live planning before development begins. Start with the Antom integration guide or speak with Antom payment experts to review your target markets and launch requirements.

Common Cross-Border Payment API Integration Mistakes

Treating cross-border payments like domestic card processing

International checkout requires more than card acceptance. Local payment methods, currencies, customer expectations, authentication requirements, and risk patterns vary by market.

Ignoring webhooks

If your system only relies on frontend redirects, order status can become unreliable. Webhooks should be a source of truth for payment status updates.

Launching without local payment method research

Payment method coverage should be mapped before development. Otherwise, the business may launch in a market where customers do not see the payment options they trust.

Testing only successful payments

A good integration must handle failure, pending status, cancellation, refunds, duplicate requests, and webhook retries. These scenarios often create the most support and finance workload after launch.

Forgetting reconciliation

Finance operations should be part of the integration plan. Transaction records, settlement reports, refunds, and fee visibility are critical for scalable cross-border payment operations.

Hardcoding market logic

Payment method availability, rules, and checkout behavior may change by region. Avoid building rigid logic that is difficult to update as the business expands.

Managing keys and environments loosely

Production keys, sandbox keys, notification URLs, and private keys should be controlled carefully. Poor credential management can create security, reliability, and launch risks.

How Antom Helps Businesses Integrate Cross-Border Payments

Antom, Ant International's leading merchant payment and digitalisation platform, helps businesses accept global and local payment methods, simplify cross-border payment operations, and support international growth through one integrated payment platform.

For developers, Antom provides integration resources such as payment APIs, checkout options, API references, sandbox tools, notification configuration, and documentation. For product, operations, risk, and finance teams, Antom supports global payment acceptance, local payment method access, payment orchestration, fraud management, reporting, settlement, and reconciliation workflows.

This combination matters because cross-border payment integration is rarely owned by one team. Developers need clear APIs and test tools. Product teams need a checkout experience that works across markets. Risk teams need fraud controls. Finance teams need reliable reports. Business leaders need payment infrastructure that can support expansion without adding unnecessary operational complexity.

If your team is evaluating how to integrate cross-border payments across multiple markets, Antom can help you review target markets, payment method coverage, integration models, risk controls, reporting requirements, and go-live planning.

FAQ

What is a cross-border payment API?

A cross-border payment API allows a business to accept payments from customers in different countries or regions through a technical connection with payment infrastructure that supports international transactions. It can support payment creation, local payment methods, status updates, refunds, reporting, settlement, and reconciliation.

How do you integrate a cross-border payment API?

A typical integration includes defining target markets, selecting payment methods, setting up sandbox credentials, implementing API calls or SDKs, configuring webhooks, testing payment scenarios, preparing risk controls, reviewing reconciliation workflows, and moving carefully from sandbox to live mode.

What should developers test before going live?

Developers should test successful payments, failed payments, pending payments, cancellations, refunds, webhook delivery, duplicate requests, invalid signatures, error scenarios, mobile checkout behavior, local payment method behavior, order status updates, and reconciliation records.

Why are local payment methods important in cross-border payments?

Customers in different markets often prefer different ways to pay. Some markets rely heavily on digital wallets, online banking, bank transfers, QR-based payments, or regional payment networks. Supporting local payment methods can improve checkout familiarity and reduce payment friction.

What role do webhooks play in payment API integration?

Webhooks allow payment status updates to be sent to the merchant backend. They are important because customer redirects are not always reliable, especially for asynchronous local payment methods or interrupted checkout sessions.

What is the difference between a cross-border payment API and a payment gateway?

A payment gateway is often focused on payment acceptance and transaction routing. A cross-border payment API may support a broader set of capabilities for international commerce, including local payment methods, multi-currency processing, authentication, notifications, refunds, reporting, settlement, and reconciliation.

How should businesses choose a cross-border payment API provider?

Businesses should evaluate market coverage, local payment method support, integration options, developer documentation, sandbox tools, webhook reliability, risk management, reporting, reconciliation, operational support, and long-term scalability.

Ready to Build a Scalable Cross-Border Payment Integration?

A strong cross-border payment API integration helps your business do more than accept payments. It supports localized checkout, improves operational visibility, reduces integration complexity, and creates a more scalable foundation for global expansion.

If your team is planning to enter new markets or consolidate multiple payment integrations, Antom can help you evaluate the right payment setup for your business model. Explore Antom developer resources or speak with Antom payment experts to review your target markets, preferred integration model, local payment method needs, risk requirements, reporting workflow, and go-live plan.